Blond Treehorn Thug: Where’s the money, Lebowski?

The Dude: It’s uh…uh…it’s down there somewhere, let me take another look.

– The Big Lebowski, 1998

Introduction

This is a very complicated case, Maude. You know, a lotta ins, a lotta outs, a lotta what-have-yous. And, uh, a lotta strands to keep in my head, man.

“Slightly lower taxes for some, similar taxes for others” doesn’t sound like an exciting policy platform. But any time we’re talking about a major U.S. tax and spending bill, the stakes are high.

Were it not for the ongoing trade war, the current debate over renewing and amending the 2017 Tax Cuts and Jobs Act (TCJA) via budget reconciliation would be the main source of investor interest coming out of Washington, D.C., right now. But as we get into the summer, it is likely to take center stage.

As Congress prepares to make the sausage over the next few months, now is a good time to assess where the bill stands, what’s in it, and what impact on the economy and markets it may have. There are too many details to cover adequately in a single piece, but our high-level views are:

- The bulk of the bill’s cost is maintaining the lower tax rates set to expire from the 2017 TCJA

- Inclusion of the debt ceiling raise will help usher the bill to passage given the catastrophe that could result from a Treasury default

- The bill is likely to provide new relief for certain taxpayers (e.g., tipped workers and social security recipients) while only cutting spending a little, meaning it will increase the deficit

- Bond markets may not fully revolt against the bill, but wider deficits in perpetuity could prevent long-term interest rates from returning to their low range during the 2010s

The U.S. economy has slowed, and policy uncertainty emanates from virtually all parts of the government. That’s a combustible backdrop for such consequential lawmaking. Filled, as it is, with inexplicable plot twists and incomparable characters, we could think of no better film to inspire us as we survey the state of play on Capitol Hill than the 1998 absurdist neo-noir classic, The Big Lebowski.

What’s going to be in the tax bill?

Look, man, I’ve got certain information, all right? Certain things have come to light.

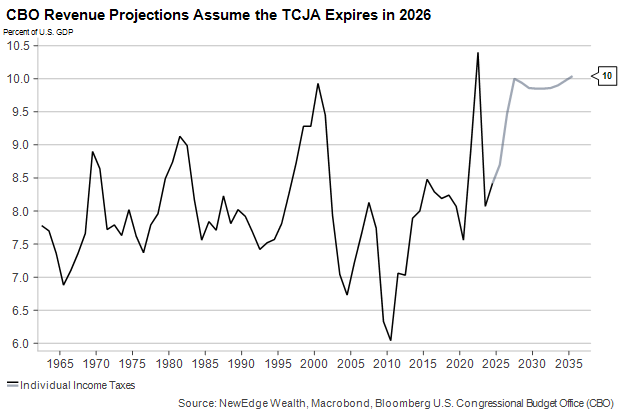

Income tax rates will go up a lot for everyone who pays them on January 1, 2026, unless Congress intervenes. Just as The Dude’s rug really tied the room together, the prospect of avoiding higher taxes unites all Congressional Republicans. Keeping individual tax rates from rising next year is Job #1 in this bill.

There was a kerfuffle this week over the possibility of tax rates going up on individuals making $2.5 million or more, which even President Trump seems to support. But Republican aversion to raising any taxes runs deep, and we do not – at this point – see the creation of a new higher tax bracket as likely.

Job #2 is making as many of the major provisions in the bill permanent. This is more challenging than it sounds given the Senate’s so-called “Byrd Rule”, which stipulates that no bill passed through the reconciliation process can expand the deficit beyond a ten-year window. The reconciliation bill will deal mainly with taxes, but it will also allocate a few hundred billion in new defense authorizations, border security, and disaster relief for areas affected by extreme weather events last year. These will make the Byrd Rule harder to abide by if the spending increases become permanent, as they tend to.

The “tax spending” parts of the bill – new carveouts and exemptions – are where things start to get fun. The current $10,000 per couple cap on State and Local Tax (SALT) deductions was one of the higher-profile TCJA tax savings measures. Now, after successful 2022 and 2024 elections, there are enough Republicans in high-tax states like New York and California to demand a higher SALT cap. Leadership may have to say, “Okay, Dude. Have it your way,” to the Blue State Republicans and agree to add this costly provision to the bill.

President Trump campaigned last year on several new specific tax carveouts and is backing them strongly now that he is in office: no taxes on tips, social security, or overtime. These are likely to be included in the bill in some form, though they may be prime candidates for “sunsetting”, meaning they could take effect in 2026 but expire at or before the end of the 10-year window to avoid running afoul of the Byrd Rule.

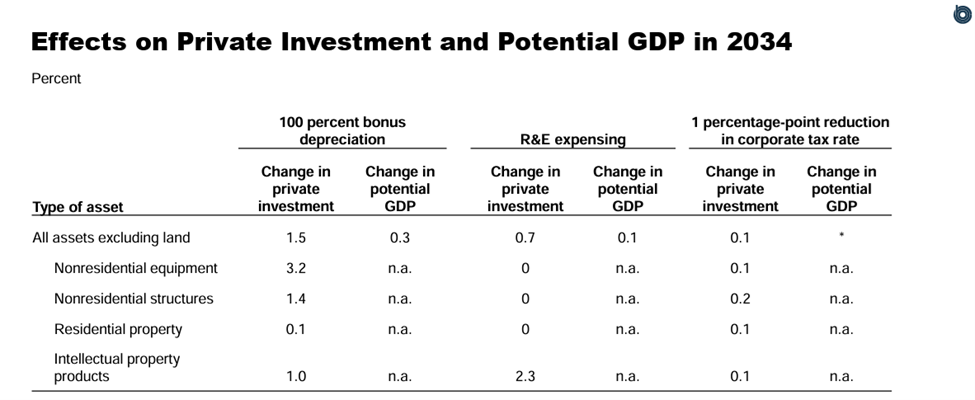

The TCJA permanently lowered corporate tax rates, but the provisions allowing companies to write off asset depreciation at an accelerated pace are currently phasing out and may be renewed in this bill. For most of the past thirty years, businesses have been able to use accelerated, or bonus, depreciation to lower current tax costs. While significant for many firms and potentially stimulative for investment, the Congressional Budget Office (CBO) does not estimate that any of these corporate tax provisions move the needle for the overall economy.

One way to avoid blowing out budget deficits with tax cuts and spending increases is to raise other taxes and cut other spending. No government initiative (save, the tariffs) has received as much attention in 2025 as the Department of Government Efficiency, or DOGE. Its mission is to find cost savings in executive branch departments and programs. So far, the bulk of its efforts have gone to canceling contracts and reducing headcount.

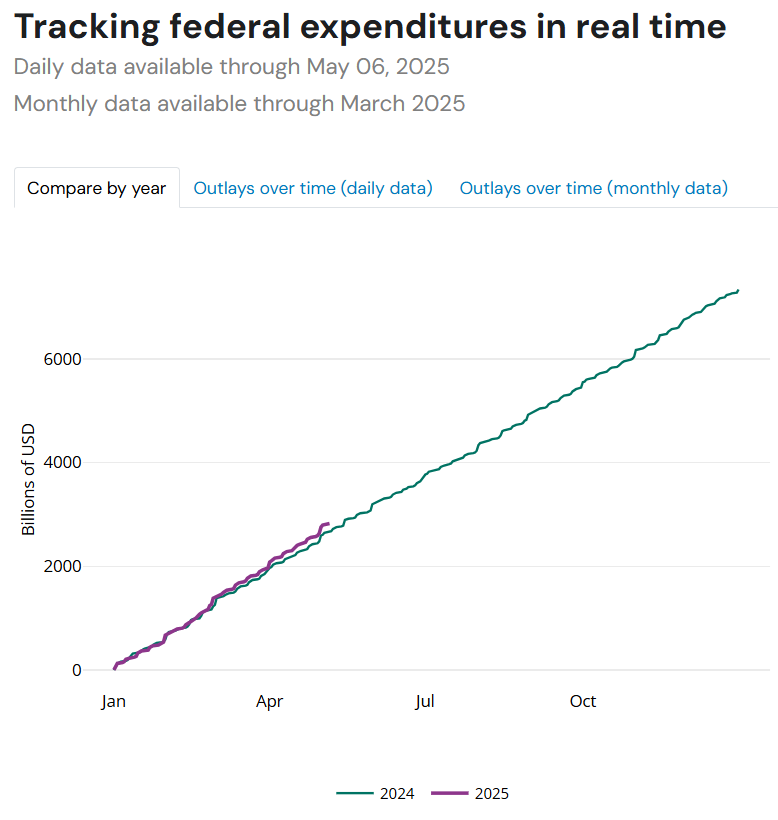

There are two problems with using the DOGE savings to offset new tax cuts and spending increases. First, DOGE cuts have not been blessed by Congress, and courts are still adjudicating the right of the executive branch to refuse to spend appropriated funds. Second, even if Congress were to codify the DOGE actions into law, it is not clear the savings identified so far amount to much in the grand scheme of things. According to the Hamilton Project, federal outlays are still running close to 10% higher than last year:

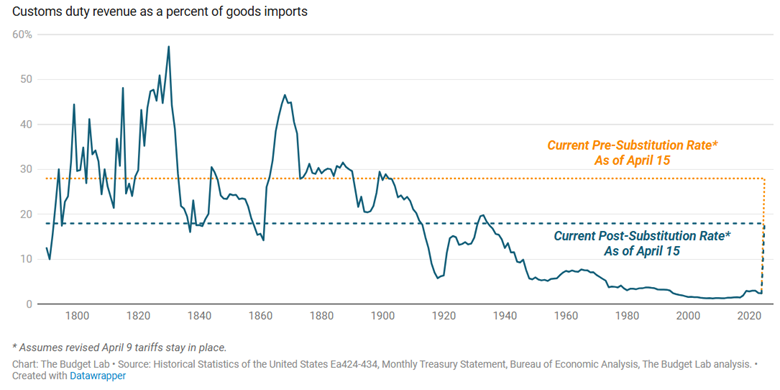

If executive spending cuts cannot deliver savings, perhaps executive tax increases like tariffs might do the trick. Tariff revenue boosted U.S. Treasury coffers as imports surged during the first quarter, and daily revenue is averaging close to $300 million per day compared to $200 million prior to April 2nd. The Yale Budget Lab estimates that the new Trump tariffs could raise close to $2 trillion through 2035 were they to stay in place. That money could be used in the tax bill if the tariffs were formally enacted into law, but that seems unlikely for now given their unpopularity.

While spending cuts are always politically treacherous, Congress will need to curb some areas of discretionary spending to make the budget math work. The two main candidates for cuts are in social assistance programs like SNAP (i.e., food stamps) and Medicaid. The clean energy subsidies passed in 2022 as part of the Inflation Reduction Act also appear to be on the chopping block.

Medicaid may not be quite the “third rail” of American politics that Social Security and Medicare are, but it’s close. House Speaker Mike Johnson has already taken some of the more controversial potential cuts (e.g., per capita caps or reimbursements to states) off the table. But work requirements for eligibility (“Are you employed, sir?!”) seem likely to be included.

The most important provision in the reconciliation bill will be a debt ceiling increase. While raising the debt ceiling has little real-world impact, not doing so could lead to an economic catastrophe. With Democrats unlikely to provide any help to get to 60 votes in the Senate, the only real chance for Republicans to pass it is via simple majority in reconciliation.

The debt ceiling’s inclusion provides helpful urgency in moving the full package to passage. While there is not yet a firm “X” date on which the Treasury will default if not authorized to borrow more, it appears to have the funds on hand to make ends meet through most of the summer. “Life does not stop and start at your convenience!” as the great Walter Sobchek put it. Whatever negotiation ploys or foot dragging members might want to employ, the debt ceiling is the ticking time bomb that could ultimately force this entire bill to hasty passage.

What are the roadblocks to passing the tax bill?

Look, pal, there never was any money.

Given the imperative to raise the debt ceiling and prevent a massive tax increase next year, the reconciliation bill may, indeed, be too big to fail. But small majorities in both chambers of Congress, including a handful of members who may not vote for any plausible compromise (“We believe in nothing, Lebowski! Nothing!”) make the path narrow and perilous. We see three major obstacles to the bill passing without major changes to its current makeup.

First, the economic environment could be very different in just a month or two. A few months of job losses and high inflation coupled with surging small business closures on account of the tariffs could lead the bill to be more focused on short-term stimulus. A weaker labor market could also make cuts to social programs impossible, leading to larger deficits.

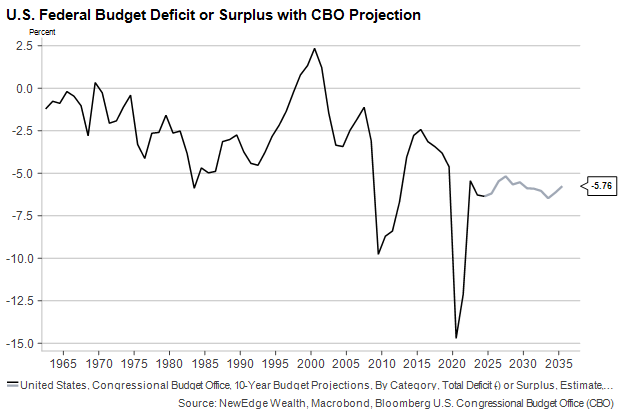

Second, even if the economy is still hanging tough this summer, the bond market could deliver a negative verdict on the bill if it seems likely to produce higher deficits in perpetuity. The current federal budget deficit is already large as a percentage of GDP given low unemployment and the absence of major military engagements. The CBO estimates that this ratio would remain in the 5-6% range were the TCJA cuts to fully expire, meaning even a simple TCJA extension would increase it to prior “crisis-era” levels.

Full TCJA expiration has never been likely and is not priced in, but a large “budget busting” tax bill could keep long-term rates higher than they would otherwise be. Even if bond investors stop short of delivering the kind of “veto” they did in the U.K. in 2022, they are influencing the legislative process to a degree we have not seen since the early 1990s. This is the era in which Clinton advisor James Carville famously said “I used to think that if there was reincarnation, I wanted to come back as the president or the pope or as a .400 baseball hitter. But now I would like to come back as the bond market. You can intimidate everybody.”

The third obstacle to passage is the Senate budget rules, which permit reconciliation bills to pass with a simple majority only if they can be scored as deficit-neutral beyond a ten-year window. Ambitions to make some of the provisions we’ve discussed permanent will require large and permanent cuts elsewhere. A slew of sunset provisions – especially on the new tax carve outs – seems the more likely path.

What’s the economic impact?

Thank you, Walter, that makes me feel very secure. It makes me feel very warm inside.

We speak to many investors who are hopeful that this tax package will provide a helpful offset to the significant tax increases that have resulted from the tariffs. Indeed, many architects of the tariff policy itself posit that tax can largely or entirely funded by trade taxes.

We are skeptical of this claim, not least because trade deals could substantially reduce revenues if they reduce tariff rates. There is also an issue of timing. Tariffs have already been in place for several months, while any fiscal stimulus from the tax bill might not kick in until next year.

We expect the tax bill to produce larger budget deficits for the foreseeable future, which will provide some fiscal stimulus to those who stand to benefit from any new tax carveouts. The centerpiece of the bill, however, remains the extension of the TCJA cuts, which would prevent severe fiscal tightening but will do little to stir any households to spend more than they were already planning to.

Will the tax bill bail out markets?

Sometimes you eat the bear, and sometimes, well, he eats you.

Isolating the market impact of a tax bill with unsettled components in an uncertain environment is challenging, to say the least. Suffice to say, long-term U.S. interest rates are currently higher than they would be if the U.S. government was planning austerity measures. But in the short term, rates will be more sensitive to economic data than long-term budget projections. This could mean the most likely path for the 10-year Treasury yield may be lower over the summer (in response to weaker economic data) and then higher into the end of the year (in response to higher deficits). The magnitude and timing of these moves will depend on the severity of the slowdown and the amount of new borrowing required to finance the tax bill.

Equity market moves are not typically correlated with tax rates or budget deficits, but failure to raise the debt ceiling or extend the TCJA tax rates would clearly not be good for risk assets. The strong U.S. equity market recovery since early April along with the stubbornly high yields on the long end of the Treasury curve point to some amount of fiscal stimulus being priced in. A larger bill seen as more stimulative might push up the U.S. dollar from its weakened position, but one that is too large might hurt the currency if it is seen as detrimental to U.S. credit quality.

Larger deficits also muddy the outlook for the Fed’s interest rate policy. They don’t teach you to ease policy in the face of wider budget deficits in Central Banking 101. But it would also be strange for the Fed to hike rates in a weakening economic environment, even if it believes fiscal stimulus is on the way.

Conclusion

You can imagine where it goes from here.

The tax bill taking shape in Congress remains a source of uncertainty for the U.S. economy and financial markets. Thankfully, the inclusion of the debt ceiling increase and the need to prevent taxes from going up in a few months makes it all but certain to pass at some point this year.

At the same time, we are concerned that investors may be incorrectly assuming that the bill as currently constituted will provide meaningful immediate help to the U.S. economy. Beyond some renewed investment incentives and a collection of new tax carveouts, the bill will lock in large but stable budget deficits over the next decade without providing a strong new stimulative impulse.

The wild card is how the economy evolves and whether a significant weakening of the labor market and the consumer may compel changes to the bill as more households and businesses require immediate aid. In that scenario, we could see increased volatility in interest rates and an uncertain response from the Fed, which would create a tricky backdrop for risk assets.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2025 NewEdge Capital Group, LLC

The post Will Congress Abide The Big Tax Bill? appeared first on NewEdge Wealth.