The Employment Situation is Up in the Air

“We’re here to talk about your future.”

From just after the global financial crisis through the high inflation of the early 2020s, the U.S. labor market has been on a generally positive trajectory. The pandemic aside, monthly payroll growth since the GFC has nearly always been positive (indeed, until the latest revision to the June report, there had been no negative months since December 2020), and the unemployment rate has moved from very high to very low. Despite having risen nearly a percent from its recent trough, it remains low to this day.

Lately, however, cracks have begun to emerge. Fewer workers are voluntarily quitting, and consumers report steadily increasing anxiety about their employment prospects. The August U.S. employment report, and the ones just preceding it, confirm that job creation has shifted into a lower gear.

Up in the Air, the 2009 film about professional consultants who travel around the country laying off workers, captured the anxiety of working in the wake of the financial crisis. While the labor market is not nearly as bad today as it was when the film debuted, general anxiety about the jobs picture has increased, making this film a harrowing rewatch. But in the wake of a poor August jobs report, we thought it was an appropriate choice to inspire this Weekly Edge.

Another Very Bad Jobs Report

“Well, life can underwhelm you that way.”

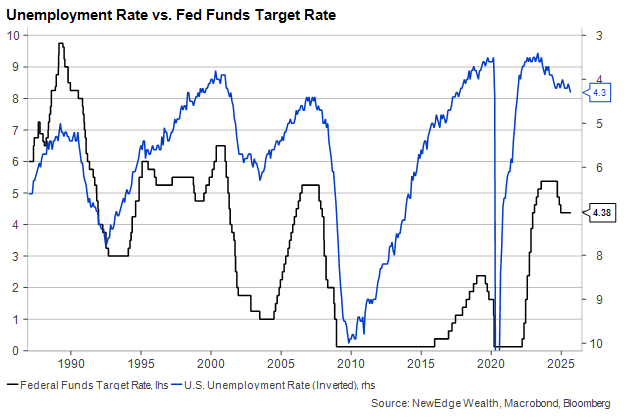

The best thing that we can say about the August U.S. employment report is that no one will accuse the Bureau of Labor Statistics (BLS) of manipulating the data to make it look good. The unemployment rate rose to 4.3% from 4.2% in July, nonfarm payroll growth was just 22,000 (vs. 75k expected), and growth over the prior two months was revised down a bit, with the 3-month average job gain running at just 29k. Average hourly earnings growth also fell short of expectations.

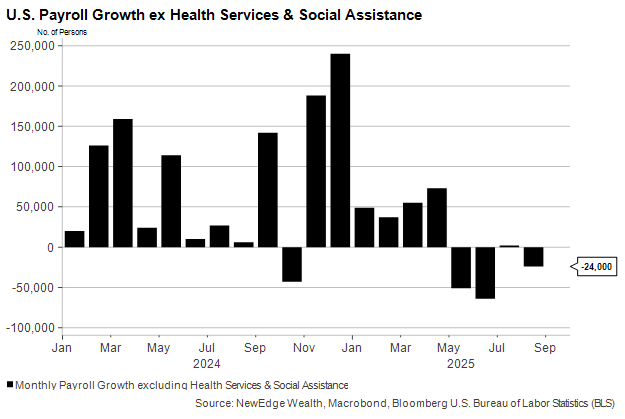

Perhaps most worryingly, for the fourth straight month, one sector (Health Services) was responsible for 100% or more of the payroll growth while most others shed jobs::

It’s impossible to analyze this employment report without acknowledging that the prior one, released last month, led directly to the BLS Commissioner’s firing. The main reason given for the dismissal was the large negative revisions to the May and June reports.

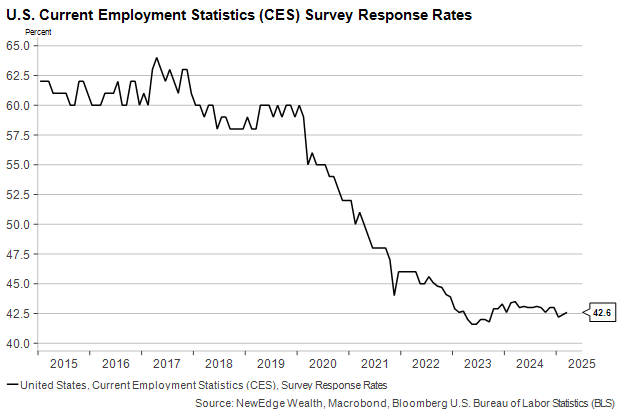

These employment reports are only as good as the responses the government agencies that tabulate them get from individuals and companies. This next chart shows the drop in companies’ response rates to the BLS surveys each month. Note the sharp and understandable drop in 2020 and the notable lack of any bounce long after the emergency subsided:

The BLS estimates total employment, not the change in employment, each month. An error of a few thousand – even a few hundred thousand – in the context of a workforce of 170 million should not be thought of as unusual, let alone evidence of incompetence or fraud.

All of that said, investors should be prepared for a further significant (and, according to economists we trust, negative) revision to total payroll gains for late 2024 and early 2025 once the BLS’ Preliminary Benchmark Revision using census data is released on Tuesday, September 9.

Labor market softness likely has further to go

“Life’s better with company.”

Even before the August jobs report dropped, it had been obvious for several months that the U.S. labor market is under some strain. Most data points show only moderate deterioration, but nearly all are weaker than they were at the start of the year. Summer labor market data has been almost uniformly bad after a hopeful start to the year:

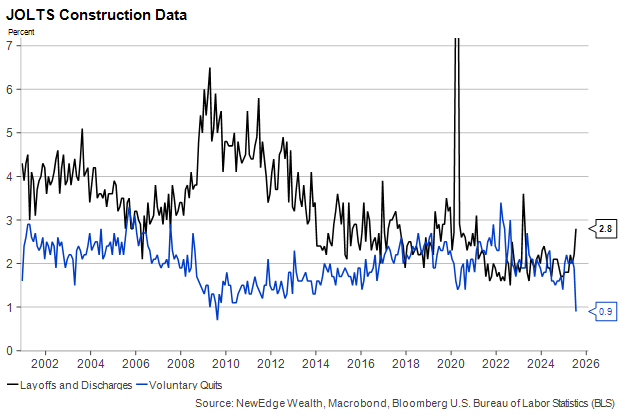

The BLS’ Job Openings and Labor Turnover Survey (JOLTS) has been showing fewer job openings, weaker hiring, fewer voluntary resignations and more layoffs for months, but the latest data contained an abrupt drop in the quits rate among construction workers just as the layoff rate in the industry has picked up:

As we wrote in last week’s housing-themed report, construction employment has remained surprisingly resilient in the face of plummeting permits and housing starts, not to mention falling home prices in many parts of the country. Commercial construction (outside of data centers) also remains sluggish. Those trends may finally be feeding through into the job market, as construction jobs fell for the third consecutive month in August.

One of the major sources of construction activity has been and remains manufacturing facilities. While growth in factory construction has stalled, activity remains elevated compared to before the passage of the CHIPS Act in 2022. But if these factories are coming online, they aren’t resulting in greater overall manufacturing employment:

Manufacturing employment has been shrinking since 2023, and weak employment sentiment in the last few ISM Manufacturing surveys indicates this weakness may continue for some time.

Consumers are becoming increasingly worried about the labor market, a trend that typically accompanies a rising unemployment rate. Household anxiety about employment can become its own source of downside economic risk if it results in higher savings and less consumption.

If we are looking for positive signs in the U.S. jobs market, we must look at something other than the monthly BLS reports. Weekly jobless claims data has shown only a very gentle rise in the number of people filing for unemployment assistance in the states, and the cumulative number of people receiving unemployment assistance, while higher than a year ago, is not increasing at an alarming trajectory:

Slow job creation for a slow-growing population might be OK

“The slower we move, the faster we die.”

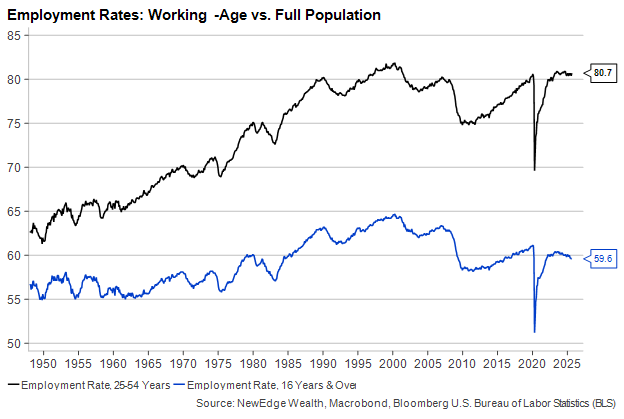

Zooming out even further, the remarkable thing about today’s labor market is that close to a record share of working-age (25-54) Americans are employed. The graph below shows that if fewer people are working than in years past (the blue line), it is mainly due to a larger portion of the population being retired.

Recent changes to U.S. immigration policy are also affecting the employment rate. A stricter immigration policy, especially one that emphasizes deportations, tends to reduce the available worker pool. And because foreign-born workers tend to be younger than the native-born population, ceasing net migration into the country also reduces the labor force participation rate. This could cause unemployment to be lower than it otherwise would be while nudging wage growth up, likely the desired effects of the policy.

Over the long run, a country’s potential growth rate depends on how fast its labor force is increasing and how quickly its workers are seeing their productivity increase. Today, both of those rates are on a downtrend compared to the last several years, which means two things. First, the rate of payroll growth needed to keep unemployment steady is quite low (though probably higher than we got in August). Second, U.S. GDP growth of 1.5% or so should be a baseline expectation for the next few years with low productivity and population growth the likeliest outcomes.

Conclusion

“Let’s just say I have a number in mind, and I haven’t hit it, yet.”

In addition to dispelling any notion of data manipulation, the other “nice” thing about the poor August jobs numbers is that they clarify the near-term path of monetary policy. Interest rates plummeted following Friday morning’s release, and market-based expectations for a Fed rate cut at the next meeting on September 19 rose above 100%, implying some chance of a larger cut, which we see as unlikely.

Where the Fed goes from there will depend on the paths of unemployment and, of course, inflation, which remains well above its target. Right now, investors are confident that the Fed will cut rates at every meeting through the end of the year, but we would still place bets on either side of that “three” number.

It’s easy to imagine a scenario in which the summer soft patch proves a blip, as it did in 2024, and the Fed only cuts once this year. But, especially after this week, it’s equally plausible that a longer string of poor jobs reports compels the Fed to make larger cuts at its Q4 meetings.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2025 NewEdge Capital Group, LLC

The post Up in the Air appeared first on NewEdge Wealth.