All we know is that we don’t know

Oasis, “The Masterplan”

Of the things from 2025 that we would like to see more of in 2026, at the top of the list is Oasis reunion concerts (maybe with even more B-side cuts, like those included on the band’s The Masterplan 1998 compilation album).

Coming in right behind the dueling Brit brothers would be another year of strong gains for the S&P 500 and healthy growth in the US economy.

Of course, we are not alone in wanting these outcomes for the US economy and global markets (though another rock band from across the pond reminds us that “you can’t always get what you want”), and we can see this popular desire for another strong year by assessing consensus forecasts for 2026.

This week’s Weekly Edge will be a brief summary of where consensus stands for the US economy, equity markets, the Fed, and the USD. What strikes us about all of these consensus estimates is that they shake out to average outcomes, such as forecasting 9% equity market returns (the long-run average annual return for the S&P 500) or 2% US economic growth (consider long-term “trend” growth). Expecting average likely reflects strategist uncertainty and a lack of desire to stick one’s neck out, meaning it is an effective sing-along to the title track from Oasis’ The Masterplan, saying “all we know is that we don’t know.” Throughout the piece, we will include screen grabs from this great Bloomberg article, which helpfully compiled Wall Street consensus across various topics.

This weekend’s analysis of consensus tees us up (there is foreshadowing about the 2026 Outlook theme here) to present our 2026 Outlook next week on Wednesday. We have long chosen to present our Outlook in the second week of January in order to use this assessment of consensus in our views for the year ahead. This allows us to sing along with The Masterplan as well, asserting that we will “take some time to make some sense of what you want to say.”

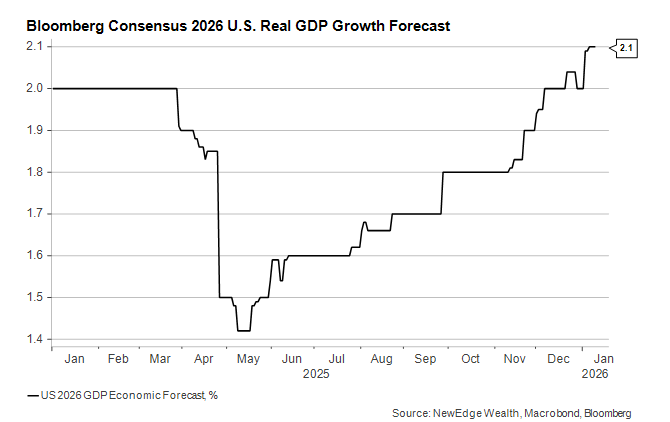

“Tell Them Not to Fear No More”: US Economy Consensus

Someone who fell asleep on January 1, 2025 and woke up on January 1, 2026 might reasonably surmise that nothing much had happened to the U.S. economic consensus while they slept. How wrong they’d be! This chart shows the wild (for GDP, anyway) forecast swings that occurred last year after the U.S. announced high and broad tariffs on imported goods in April.

Ultimately, the tariffs did not end up being nearly as high or broad as first billed. Durable corporate profit margins and persistent consumer spending growth through the summer caused economists to re-revise their thinking for both 2025 and 2026. The current consensus forecast of 2.1% reflects expectations that consumer spending growth will decelerate to 2% but that more of that growth will come from domestic rather than imported items.

There wouldn’t be anything particularly exciting about another year of 2% GDP growth for the United States, but recent history suggests that it’s more than good enough to help equity markets power ahead to another successful year and keep the labor market roughly in balance.

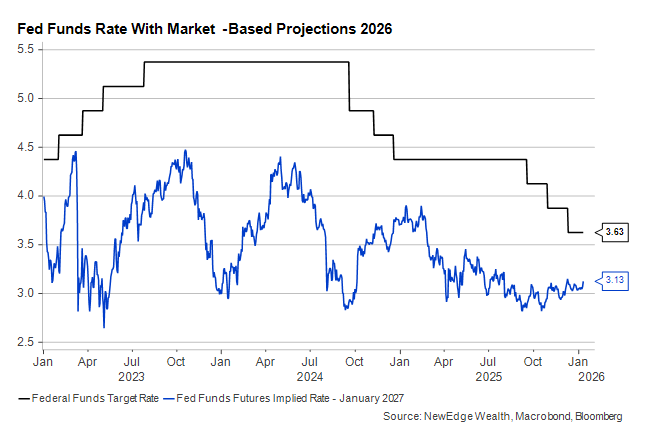

“You Know They’re Gonna Go Which Way They Wanna Go”: Fed Consensus

Another year of 2% growth might not provide much greater clarity for a Federal Reserve that faces the prospect of being on the wrong side of both of its mandates. Inflation is still too high by the Fed’s own standards while unemployment, while low, has been gradually rising amid unusually weak job creation.

The black line on this chart shows the midpoint of the Fed’s target range while the blue line shows the market’s expectations – going all the way back to 2023 – of where policy will be at the start of 2027. Four years is a long time in the future to make monetary policy projections, as the oscillation in the blue line shows.

Markets have, for now, settled on almost exactly two more rate cuts as the baseline expectation for the Fed this year, with the first cut fully priced in for June. By this time, there will almost certainly be a new Chair in place, but there will also be six more months of economic data to chew on.

That the most recent forecast from the Fed itself calls for only one rate cut may not be of much interest, because a) the composition of the voting committee will change, perhaps significantly, over the next few months; and b) most of the Fed’s members are data dependent.

For the Fed to remain on an easing bias without actually cutting below 3%, inflation would need to remain tame and unemployment would likely have to rise further…but not a lot further.

“On a Ship of Hope Today”: Equity Market Consensus

Even the bears are bullish in 2026, with no major Wall Street strategists calling for a down year in 2026.

The chart below shows the range of expectations for the S&P 500 (as of 12-29-25). The average year end forecast equates to ~9% gains for the fully year, which is line with the last century’s average annual return for US large-cap equities.

There is an important reminder here, which is that the S&P 500 has rarely experienced “average” returns, meaning 8-10% returns are no more common than any other 3-point range for market returns. In fact, single-year returns for the S&P 500 tend to be more extreme, with average positive years up much more than the total average of both up and down years (see the analysis here, which calculates the average positive year returning 21% and the average negative year returning -13%).

Breaking down the S&P 500’s expected return, consensus is expecting strong EPS growth ($310, +15% YoY) to be the key driver of returns. This implies slight PE multiple compression from the high starting point of 22x forward.

Note that despite these broad expectations for a fourth year of positive S&P 500 returns, Deutsche Bank’s Consolidated Equity Positioning Index is still just in the 53rd percentile, suggesting that institutional investors have not quite put their money where their bullish mouths are.

Looking to leadership, consensus is calling for a “broadening out” of leadership to include more S&P 500 sectors outside of concentrated tech/Mag 7 leadership. After the strong performance of international markets in 2025, analysts are broadly positive on non-US markets, as seen in the Bloomberg snippet below. Which is a great segue to looking at the outlook for the USD next.

“Sail Them Home With Acquiesce”: USD Consensus

One of the starkest contrasts between the 2026 and 2025 consensus is the expectation for the USD.

At the start of 2025, consensus was resoundingly bullish on the USD, with analysts citing “America First” policies and strong domestic growth that would drive further appreciation in the greenback. Looking back, the problem with all of these positive proclamations for the USD was that positioning had already fully reflected this confidence in US dollar dominance, with the chart below showing record long positioning for the dollar at the start of 2025. This crowded long positioning proved to be the fuel that drove the USD decline from January to June 2025, when positioning eventually got to extreme short levels.

Today, analysts are resoundingly calling for a weaker USD in 2026.

The challenge with this expectation is that positioning is likely not going to be the fuel that drives further USD weakness from today’s levels. The positioning chart above shows IMM positioning now short/negative for the USD. Instead of fueling a dollar decline, positioning could actually contribute to a dollar rally from today’s levels.

We think one of the big surprises for 2026 that could catch consensus off guard is a period of USD strength, partially driven by this positioning dynamic. Note that a strong USD could tighten financial conditions in the US and challenge non-US equity relative performance.

“I’m Not Saying Right is Wrong”: Conclusion

One of the most important lessons from the last 4 years of market returns is that understanding where consensus positioning lies is vitally important to anticipating the potential future progressions of markets. Narratives inevitably become dominant and one-sided, but when positioning gets just as one-sided, it can spell trouble for the returns of these crowded consensus trades. This is why assessments of both consensus narratives and positioning to understand where both can be most surprised as we progress through this new year.

We hope that you can join us on Wednesday for our Outlook presentation, where we will dive deeper into these topics and much more. You can sign up below:

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2025 NewEdge Capital Group, LLC

The post The Masterplan appeared first on NewEdge Wealth.