I’ve got the gift of one liners

And you’ve got the curse of curves.

– “The Curse of Curves”, Cute is What We Aim For

Behold the humble yield curve.

This simple display of the yields of the various maturities of Treasury bonds, ranging from shortest to longest, was once lauded as a reliable recession indicator but is now somewhat derided as a false prophet of doom.

However, instead of casting the yield curve into the discard pile of “broken economic indicators in the post-COVID world” (there are quite a few of them!), we think the yield curve remains a fascinating way to encapsulate a broad range of drivers/concerns/factors that are swirling in the minds of economy and market watchers.

Said another way, despite not being the fool-proof recession indicator it was once thought to be (yield curve “inversions” have occurred before every recession in recent history, but falsely flashed recession signals in 2022-2023), the yield curve gives us a window into how the market is perceiving big topics like the outlook for growth, inflation, fiscal dominance, Fed independence, and more.

To understand how this humble chart can tell us so much, it is helpful to start with the quick basics of the yield curve to give us a framework for our broader interpretations of its messages. We will then take a look at the messages that today’s yield curve is sending about these big topics listed above. All of this will be set to the obscure orchestration of Cute is What We Aim For’s Myspace Music-era “hit”, “The Curse of Curves”.

“The Inside Lingo Had Me At Hello”: Yield Curve Supply and Demand Framework

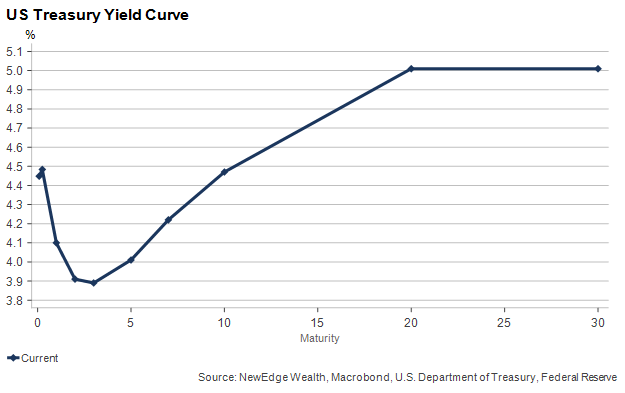

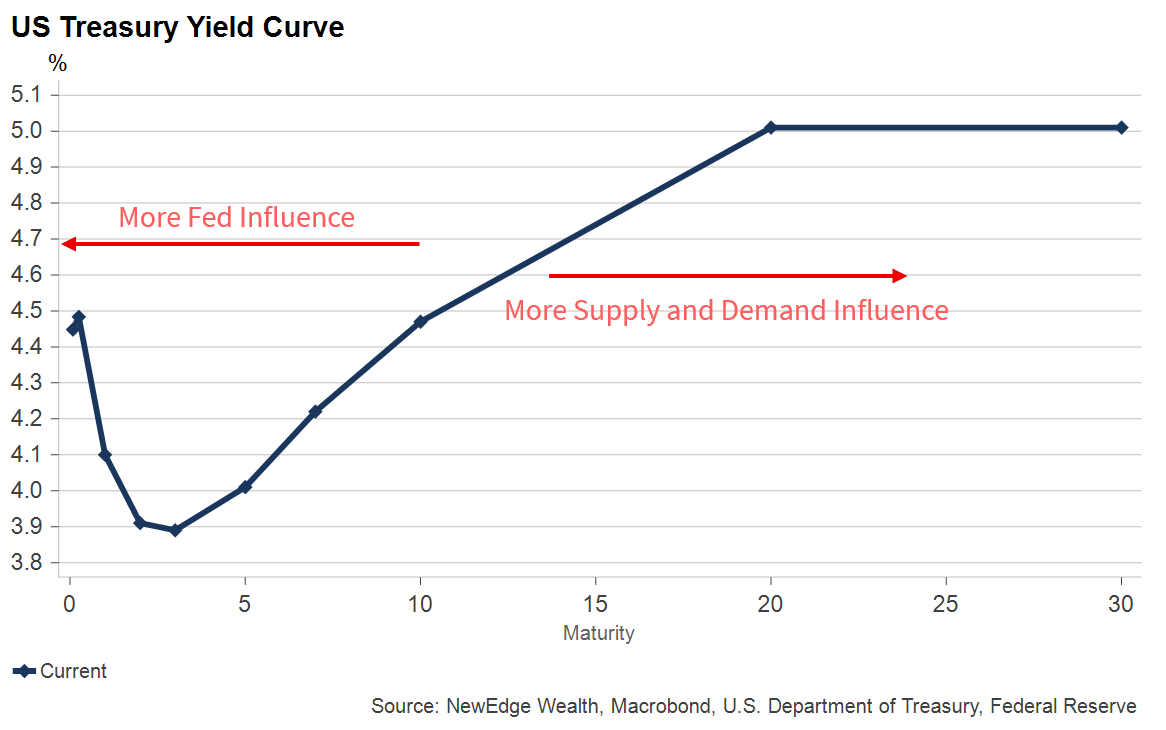

As mentioned above, the Treasury yield curve is a chart that shows yields across a range of maturities going from shortest (one-month bills) to longest (30-year bonds).

For today, we will not go through the basics of what different slopes and contortions of the yield curve mean (for a helpful overview of “normal” and “inverted” yield curves, see here). Instead, we will focus on understanding what influences these yields at various maturity dates.

At the risk of oversimplifying, one way we think about the yield curve is that the shorter the maturity date, the more yields are influenced by Fed interest rate policy, while the longer the maturity date, the more yields are influenced by other factors that we will broadly bucket into an “supply and demand”.

The Fed Funds Rate is set by the Fed and is the shortest-term, overnight rate that banks lend to each other. So, at the start of the yield curve, the 1-month Treasury bill will be roughly equivalent to the Fed funds rate. As the maturities get longer, the more expectations of what the Fed will do in the near future are reflected.

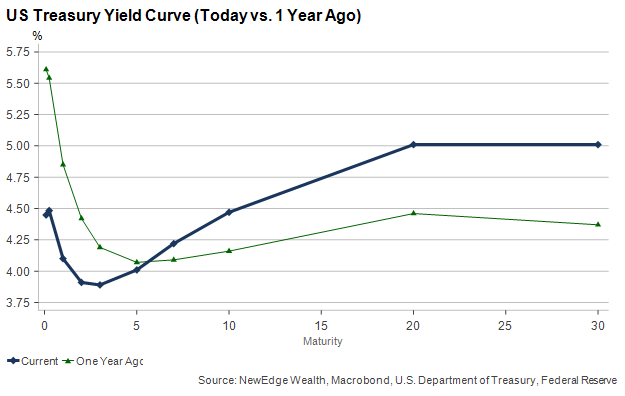

Seen in the chart above, the 1 and 3 month bill rates are effectively at the Fed Funds rate, but then the curve drops lower as it reflects the expectations that the Fed will be cutting its Fed Funds Rate in the coming years.

As you move further out the curve and it turns higher in the chart above, around the 5-year mark, this is where we begin to see influences outside of Fed interest rate policy begin to have a bigger role. Note the path forward for interest rate expectations do still influence longer maturity yields, meaning if the market thinks that the Fed will keep rates low for a long time, like in the “secular stagnation” era post the Great Financial Crisis, long-term yields are likely to be lower as well (this is referred to as “real rate expectations”).

The “inside lingo” of the bond market uses the language term premium and inflation expectations to capture these other influences to longer yields, but we like a simple, ECON 101 distillation to “supply and demand”.

(Remember our ECON 101: holding all else equal, when supply increases prices fall, so in bond math, prices falling means yields are rising. When demand increases prices rise, so in bond math, prices rising means yields are falling).

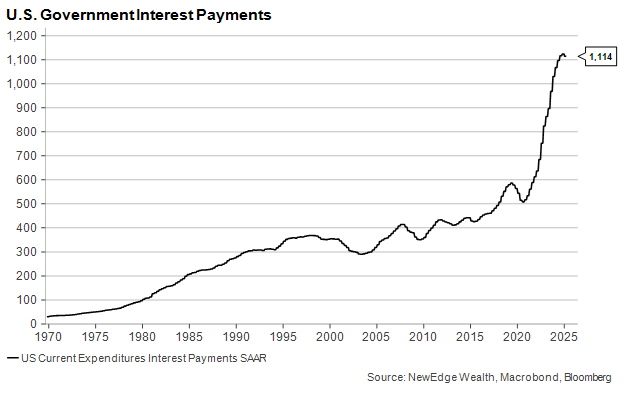

On the supply side of the equation, we begin to consider how many bonds the Treasury will have to issue in order to fund itself. If this supply of new bonds increases by more than the market can tolerate, yields will rise, like what was experienced in 2H23 when Treasury slightly increased longer term bond issuance and yields rose by over 150 bps on the 10-year Treasury. Looking forward, supply is expected to increase meaningfully in the U.S. in the coming years in order to fund the $3 trillion+ deficit expansion of the One Big Beautiful Bill.

On the demand side of the equation, we begin to consider what factors will drive demand for bonds from investors. Demand for bonds will typically increase, meaning yields will fall, when the outlook for economic growth is more uncertain or dire (this is your typical “flight to safety” into bonds in the lead up to a recession, as investors chase the safety and stability of lower risk assets). Conversely, demand for bonds will typically decrease, meaning yields will rise, when the outlook for growth is more robust (also reflected in forward interest rate expectations for higher Fed rates) and/or the outlook for inflation is hotter (because inflation erodes the value of the bonds’ fixed coupons).

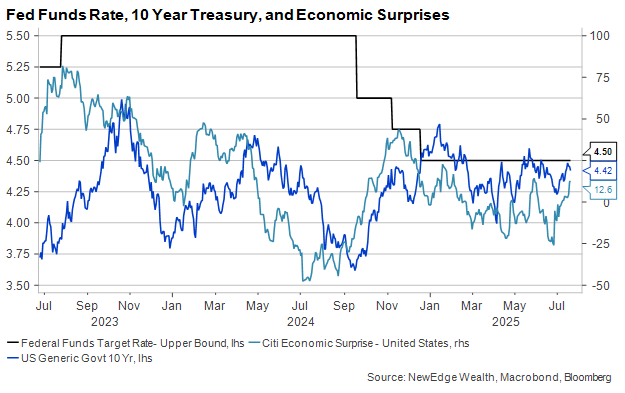

There is a great recent example of the Fed’s dampened influence on the longer end of the yield curve. In 2H24, the Fed cut interest rates by 100 bps, but the long end of the yield curve, shown below with the 10-year Treasury yield, rose 100 bps in response. The important context here is that as the Fed was cutting rates, the U.S. economy was improving and growth forecasts were rising, as captured by the teal line showing economic surprises shooting higher.

A better economy, with rising forecasts, reduced demand for save haven assets like Treasuries in 2H24, thus the yields rose, with the opposite being true in the prior months, with yields falling as economic data was disappointing. To use a tag line from Bloomberg TV: “context changes everything.”

There is one more important player in the demand equation, and that is the Fed as a price-insensitive buyer. For example, even though Treasury supply surged in 2020 to fund COVID relief programs, yields fell through the summer as the Fed’s quantitative easing gobbled up this increased issuance (the Fed expanded its balance sheet by $4 trillion in 4 months in 2020). This is an important consideration when thinking about the next recession, which will most likely see increased Treasury supply to fund even wider deficits than today’s 6.3% to GDP, but could be overwhelmed by the Fed’s bond buying.

So, now that we have set our basic framework, let us turn our eyes to today’s Fed expectations and supply and demand dynamics to help us get a read into the market’s growth and inflation expectations, along with concerns about Fed independence and fiscal dominance.

“I Want Someone Provocative and Talkative”: Fed Expectations

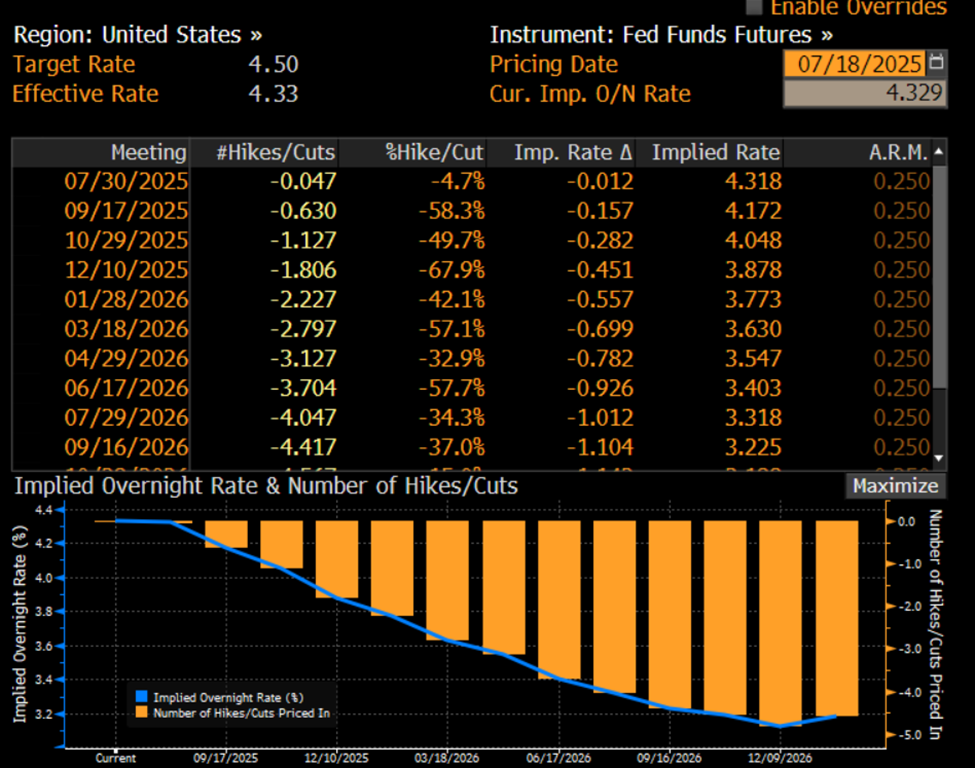

As we noted above, the market is expecting the Fed to begin cutting rates in the relatively near future, with the World Interest Rate Probability (WIRP) screen from Bloomberg showing the probabilities of rate cuts at future Fed meetings.

Notably, these probabilities for imminent rate cuts have been falling in recent weeks as growth and employment data in the U.S. have remained more resilient in the face of tariff uncertainty. Our view has been that this Fed will remain on hold until the labor market data shows greater signs of weakness due to the uncertainty about the future path of inflation in this new tariff regime.

We emphasize this Fed, because of the chorus of calls, led by President Trump, that Powell is keeping interest rates too high and that he should be replaced.

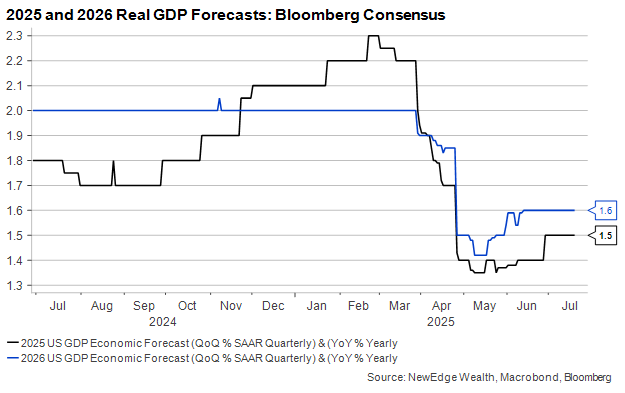

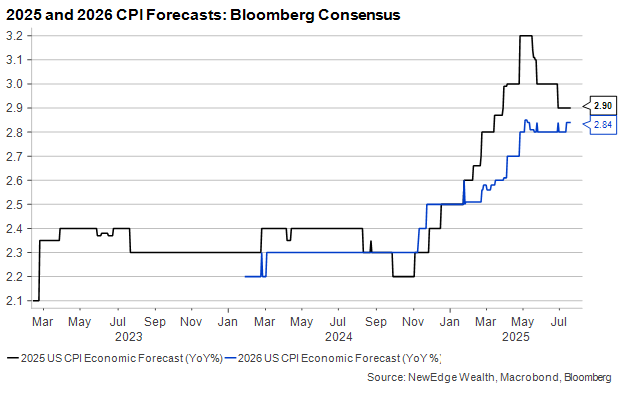

Even as growth forecasts remain healthy, though slightly below trend, as seen in the first chart below, and inflation forecasts have CPI remaining above the Fed’s 2% target through 2026, as seen in the second chart below, the market is pricing in four rate cuts by this time next year, seeing a Powell replacement as likely to deliver on the President’s rate cut desires.

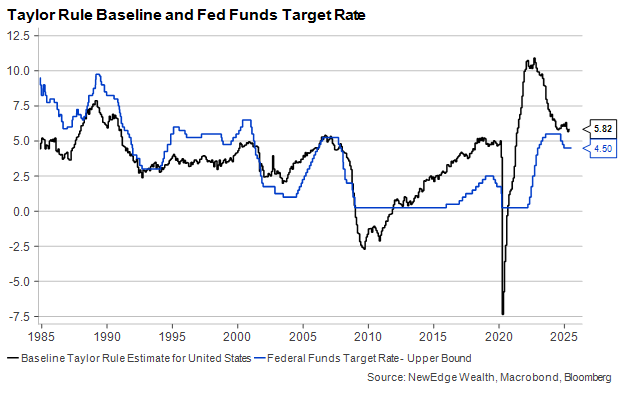

Seen another way, as Ernie Tedeschi pointed out in a Bloomberg Law article this week, based on today’s economic backdrop using the Taylor Rule (a formula to determine where rates should be given growth and inflation), the Fed’s current policy stance does not look too tight and is even below where the Taylor Rule suggests Fed policy should be set.

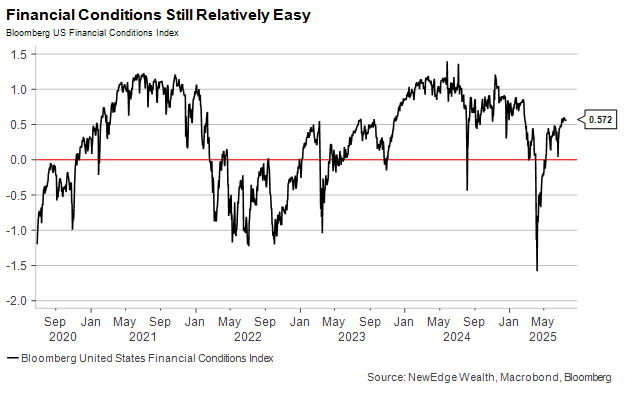

We can see this from yet another angle of broad financial conditions, which include inputs like equity valuations and credit spreads. Current financial conditions remain in easy/stimulative territory, which suggests that neither the equity nor the credit market is screaming that the Fed needs to cut rates because the economy is at risk of imminent decline. Of course, the stock and credit markets are not perfect discounting mechanisms and have often been complacent near economic peaks (we’re looking at you 2007).

This is not to say that the level of interest rates is not weighing on economic activity in certain areas, with housing being the most prominent victim of high rates (though housing is more driven by long-term rates, which as we argued above are less sensitive to the Fed’s interest rate policy). Further, for smaller businesses that tend to borrow from banks (and increasingly private credit lenders) at a floating rate, today’s high Fed Funds Rate is certainly a burden.

But Trump is not demanding that the Fed needs to cut interest rates because the economy is weak (that would be a dangerous admittance), but instead that cuts need to come in order to relieve funding pressure on the Treasury. This, in combination with Treasury Secretary Bessent’s discussion of focusing Treasury issuance on shorter-term bills, has raised concerns about how a deterioration in Fed independence and regulatory capture increases risk of future inflation, ushers in an era of fiscal dominance, and potentially erodes the attractiveness of U.S. debt across the curve.

These are sticky and complex issues, which we are sure to explore in greater detail in the coming weeks, but for now, let’s explore how the potential loss of Fed independence (Trump gets a new “provocative and talkative” Fed chair/board of governors) could impact the supply and demand dynamics impacting the yield curve.

“And We Go Where the Money Goes”: Supply and Demand Dynamics

Over recent quarters, we have been arguing that a loss of Fed independence and a potential over-easing of interest rate policy could result in a Zoo Steepener of the yield curve, where the front end experiences a bull steepener (bonds prices rally and yields drop) on expectations for rate cuts but the long end experiences a bear steepener (bond prices fall and yields rise) on reduced demand for bonds due to higher inflation/higher growth/greater concern about Fed independence.

We have already seen a Zoo Steepener over the past year, as seen in the chart below that shows a lower front end of the curve and higher long end of the curve.

Our key message is that running a hot fiscal policy with large deficits, plus potentially over-easing interest rates by a politically captured Fed, runs the risk of reducing demand for bonds (thanks to higher inflation, higher growth, and greater policy uncertainty) just at the time that supply is set to increase in order to fund said deficits. This scenario translates to a risk of higher long yields where these supply and demand factors are the dominant influence on yields.

We see this Zoo Steepener as a bad scenario for the U.S. economy, or a true “curse of curves”, as the falling front end would reduce cash interest income for savers (hurting high income consumption growth) and the rising back end would keep housing activity depressed.

“Are You Perspiring From the Irony?”: Conclusion

Treasury Secretary Bessent has been vocal that he wants and expects lower yields across the yield curve, with a target of 3% on the 10-year. We think the policy mix of increased deficits, potentially over-easy captured Fed policy, and stagflation-lite tariff and immigration impacts, all make this target of lower long end yields difficult to achieve. Instead, this policy mix runs the risk of pushing rates higher instead, exposing the U.S. economy to “the curse of curves” Zoo Steepener as front end rates fall and long end rates rise.

Of course, the context of growth will be important for the path forward for yields, with any notable weakening in the U.S. economy and labor market setting the stage for both Fed interest rate cuts and increased demand for safe haven assets like long Treasuries.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2025 NewEdge Capital Group, LLC

The post The Curse of Curves appeared first on NewEdge Wealth.