They will see us waving from such great heights

Come down now, they’ll say

“Such Great Heights”, The Postal

A few weeks ago, we wrote about the importance of earnings as a major driver of this US equity rally, asserting that twelve month forward S&P 500 earnings estimates making new highs set the stage for the S&P 500 itself to make new highs.

Of course, when talking about equity prices, there are two components: earnings and valuations (much like how there were two distinct, but distant, components to The Postal Service in Ben Gibbard and Jimmy Tamborello).

But as rising earnings provide some fundamental solace to investors looking at S&P 500 price levels, high valuations have been a source of persistent consternation.

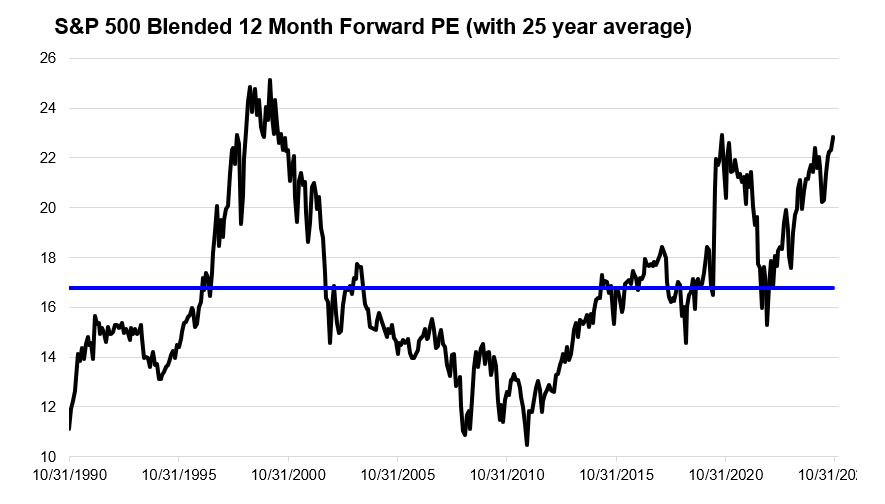

The S&P 500’s full valuation, waving at us from such great heights at 22.8x forward, is expensive by all definitions (relative to its own history, relative to other equity markets, and relative to other assets, like bonds), but the reality is that the S&P 500 has been expensive for quite some time and this richness has not yet acted as dampener on returns (we have written extensively about how valuations are not a helpful timing tool and how valuations impact on forward returns is highly path dependent).

This raises the question as to when this fulsome valuation will matter to equity returns. We think the answer to this is less about the level of valuations that will eventually matter and more about the conditions under which high valuations will begin to matter.

Said another way, certain conditions create a backdrop for valuations to expand while other conditions create a backdrop for valuations to contract. These conditions can push valuations to extreme levels (high or low), with the level of valuations becoming more relevant when these conditions change. We argue that valuation levels should be seen as amplifiers of potential price moves when conditions change (for example, if valuations are very high and conditions change, the potential downside is greater than if valuations were more reasonable).

We think these conditions for valuation expansion in recent years have been abundant liquidity, occasional offsides positioning, rising growth forecasts, and a powerful technology narrative (similar to our emo assessment of valuations this time last year).

The presence of all of these conditions has allowed the level of the index’s valuation to press back to multi-generational highs (despite cries from forecasters saying “come down now”), whereas if any of these conditions were to change in meaningful ways, we could expect valuations to contract meaningfully.

We think this is an important set of observations because it can help to prevent investors from falling prey to the four more dangerous words in finance: it’s different this time.

When valuations reach such great heights, investors scramble for reasons to justify the heady levels and argue that we are in a “new paradigm”.

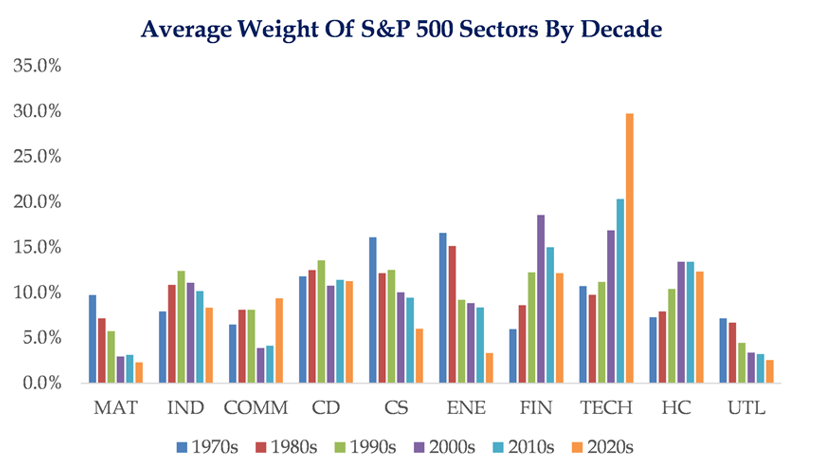

Examples of this include arguments like this Bloomberg article asserting that if you remove all the expensive names, the index isn’t that expensive (!), or that technology will provide such a huge boost to productivity and earnings growth that valuations aren’t that high today, or how today’s greater weight of high quality technology names in the index makes historical comparisons of valuations less relevant (see the chart below).

All these arguments can carry some truth, but there is danger in being wedded to them, mostly if the conditions we described above change.

To put it simply, valuations can remain elevated as long as liquidity remains abundant, growth forecasts continue to be revised higher, positioning has room to get more overweight, and tech narratives capture the hearts and minds of investors. If any of these conditions were to change in a meaningful way, such as earnings estimates being cut or liquidity receding, we would expect valuations to contract.

As Ben Gibbard reminds us that “everything looks perfect from far away”, we think it is important to look at valuations dispassionately and not get wedded to alluring narratives about new paradigms.

Through year-end, we do not see evidence that these conditions we outlined are going to become less supportive of valuations, however we will remain vigilant as we enter 2026, assessing signs that liquidity could become incrementally scarcer, earnings estimate revisions could level out, positioning could become fully overweight, or that tech dreams could fade. This suggests a continued levitation of valuations in the near term, noting that the higher heights that valuations reach, the greater the downside could be amplified if these conditions change.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2025 NewEdge Capital Group, LLC

The post Such Great Heights appeared first on NewEdge Wealth.