Catching up with Bonds

“Would you say you’re feeling low?”

With all the excitement in the equity market these days – Solid Q2 earnings! Silly stocks! AI mania! – it’s easy for bonds to get lost in the shuffle. The wild interest rate swings in the opening years of this decade have given way to a long period of elevated but stable yields, which has important implications for how we design bond portfolios.

The inspiration for our thoughts this week is “The Best of What’s Around”, the opening track on Dave Matthews Band’s 1994 debut studio album. Bonds may not end up being the “best” asset class over the next eighteen months, but we believe investors still have many reasons to own them: attractive yields, an improving diversification benefit, and a friendly macro outlook, to name a few. In particular, we want to stress diversification within fixed income portfolios, “so we can pull on through” regardless of how the larger picture macro unfolds.

Bonds’ 2025 Performance has Been…Pretty Good, Actually?!

“You and me had a better time than most can dream”

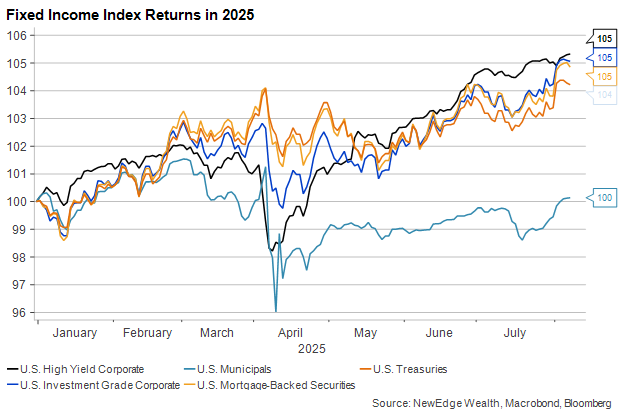

Admittedly, our expectation coming into 2025 for interest rates to move in a wide and choppy range has not yet borne out. The 10-year Treasury yield currently sits near the bottom of the narrow 4.2% to 4.6% range it’s been in since mid-April. But this year’s cumulative decline in rates – and credit spreads – has created a friendly environment for taxable fixed income returns:

The obvious exception on this graph is municipal bonds, which have traded with their usual tight correlation to U.S. Treasuries and Corporate bonds but have faced headwinds from liquidity concerns – particularly in April – and surging issuance. Higher supply coupled with merely stable demand means lower prices. Coupon returns have barely offset market losses so far this year.

For the taxable market, however, it’s been easier pickings. Setting aside the April mess (from which most sectors swiftly recovered) the macro backdrop has been extraordinarily friendly to bonds this year. Companies do not appear to be under much financial stress, and decelerating growth has helped push rates lower across just about every maturity:

Scenarios

“Whatever tears at us, whatever holds us down”

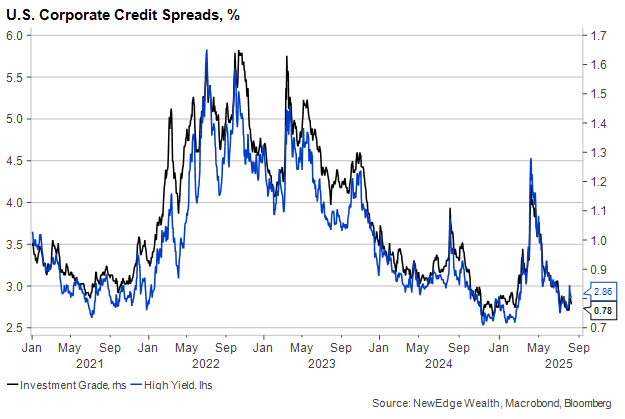

Fixed income returns have improved dramatically since 2022, but the memory of that year continues to impair investor’s appetite for the asset class. Fortunately, we do not foresee anything approaching a repeat of that year, even with the U.S. deficit ballooning and inflation creeping back up. But there is certainly potential for a wide dispersion of performance among segments of the bond market depending on what happens to growth, inflation, and economic policy over the next 18 months.

Here are what we see as the most likely scenarios along with some fixed income positioning that should perform well (or not well) in each:

Inflation on the rise: A durable rise in inflation could prevent the Fed from cutting much. Loans and cash would benefit initially, but long-term rates could eventually begin to fall in the event financial conditions tighten too much. Spread duration is a risk even in a “mini” version of 2022.

Everything goes as expected: Long-term rates could stay high even if the Fed cuts a few times at the short end. Investors holding longer-duration securities could clip coupons, but returns on shorter-duration and/or floating-rate securities could fall. Credit spreads might stay tight provided the economy remains upright.

Growth weakens further: The recent bull steepening of the yield curve could revert to a flattening or inversion if risk aversion takes hold amid acute economic weakness. Higher-quality, longer-duration bonds would likely outperform in the short run even in a recession that required deficit-expanding fiscal response.

Building a Bond Portfolio for 2025-26

“If you hold on tight to what you think is your thing, you may find you’re missing all the rest”

Building a portfolio based on past performance tends to produce suboptimal results going forward, which is why we went through the scenario analysis in the previous section. While a “muddle through” continuation of the status quo is our most likely scenario, the risk of a more material slowdown is roughly balanced with the risk of inflation continuing its rise and thwarting the expected rate cuts.

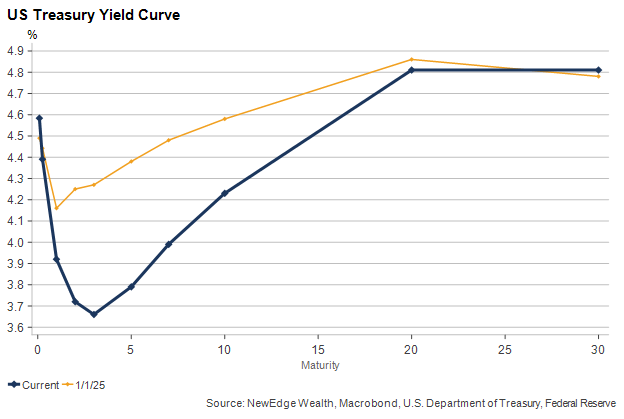

The yield curve is not as flat as it was six months ago, but getting a 4.5% yield holding taxable, investment-grade securities is achievable in several ways.

- First, we see opportunities in securitized credit, including ABS and MBS, where spreads have not compressed below their 2021 lows as corporate spread have.

- Second, an allocation to short-duration instruments like CLOs should do well in the event inflation remains sticky, the economy reheats, and the Fed continues to disappoint investors looking for rate cuts.

- Third, the steeper curve means investors are being paid more to hold longer-duration positions. While longer-maturity bonds’ prices are more susceptible to rising rates, they tend to rise during periods of economic weakness and avoid the reinvestment risk that comes from holding cash in a falling rate environment.

Each of these positions would likely be the best-performing segment of the market in one (but no more than one) of the scenarios we outlined in the previous section. This is why we are targeting a balanced approach to taxable fixed income.

Positioning Bonds in a Portfolio

“Turns out not where but who you’re with that really matters”

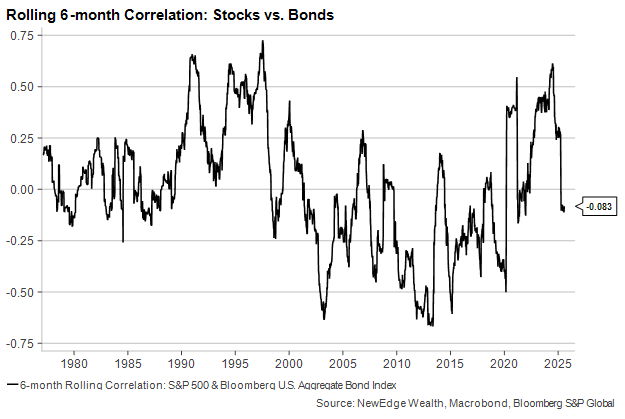

The major complaint about bonds since 2022 has been that they’ve lost their ability to diversify against losses in the equity market (not that there have been many of those over the past three years…at least many that lasted long). Stocks and bonds took a synchronous tumble that year as inflation bit the global economy and global central banks quickly moved monetary policy from accommodative to restrictive territory.

Things have begun to change. While the Bloomberg U.S. Aggregate Bond Index has not recaptured its peak diversification power from the QE-filled 2010s, its correlation to the S&P 500 has crossed into negative territory for the first time since 2021:

High and steady yields have been one factor helping to reduce the correlation between stocks and bonds. The more of the return on bonds that comes from the coupon (with less coming from market volatility), the less that return will be correlated to stocks. Bond yields are up considerably from their starting point in early 2022 and, indeed, from the entire 15-year period prior to that.

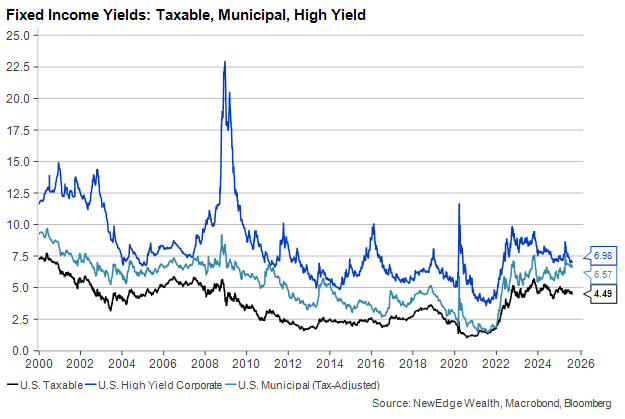

Investment-grade municipal bonds, looked at on a tax-equivalent basis for investors in the top income tax bracket, offer particularly attractive yields following this year’s underperformance. Taxable investors can swap out of High Yield Corporate Bonds (rated from BB to CCC or lower) and attain a higher yield in municipals (rate AAA to BBB) on a tax-equivalent basis.

Of course, even a 7% yield may fail to keep pace with stocks in an average year. Indeed, it’s unusual for bonds to outperform stocks for more than a few quarters absent a recession, and our base case is for a “muddle through” macro environment that will likely permit equities to stay a step or two ahead of fixed income over the balance of 2025.

Conclusion

“If nothing can be done, we’ll make the best of what’s around”

Building bond portfolios is not a flashy business. We emphasize quality and balance in our approach to building fixed income allocations, especially in today’s environment in which many different types of risk – reinvestment, liquidity, duration, credit – are providing similar risk premiums. Some of these risks will help returns over the next year while others are certain to detract from performance. Not yet knowing which will be which, we believe it is best to allocate to a variety of sectors, spreading the risk as evenly as we can.

A sudden widening of credit spreads or an abrupt reheating in economic data would likely cause us to re-evaluate our tactical stance, but while we remain in the Summer of Mudd, our preference is to stay balanced and wait for more news.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2025 NewEdge Capital Group, LLC

The post Make the Best of What’s Around with Bonds appeared first on NewEdge Wealth.