The time to hesitate is through

“Light My Fire” – The Doors

As equity markets enter the final quarter of 2024, treading cautiously and digesting the best start to an election year on record, investors are hoping third-quarter earnings results will, as Jim Morrison sang, “light my fire” and provide the fuel for further upside to close out the year.

In our view, this will be a critical corporate earnings season, where analysts and investors will have to square lofty valuations and expectations with the reality of a potentially slowing economy and continued pressures on profitability. Ultimately, solid fundamental performance and guidance could provide a much-needed positive catalyst, generating support for today’s elevated valuations and allowing markets to close out 2024 with continued momentum.

As the chart below illustrates, long-term price appreciation in equities is almost entirely driven by underlying earnings growth, one of the reasons why the forward earnings outlook remains a critical consideration in evaluating the path of the S&P500. While “profits drive price” in the long run, in shorter time periods, price appreciation can often outpace underlying earnings growth, which is largely influenced by the expectations of future profit generation, as we have seen over the past year. With the S&P500 having gained 40% since the October 2023 lows (60% of which has come from multiple expansion), we believe healthy underlying earnings growth in the coming quarters will be vital if markets are to continue their positive momentum.

Setting The Table

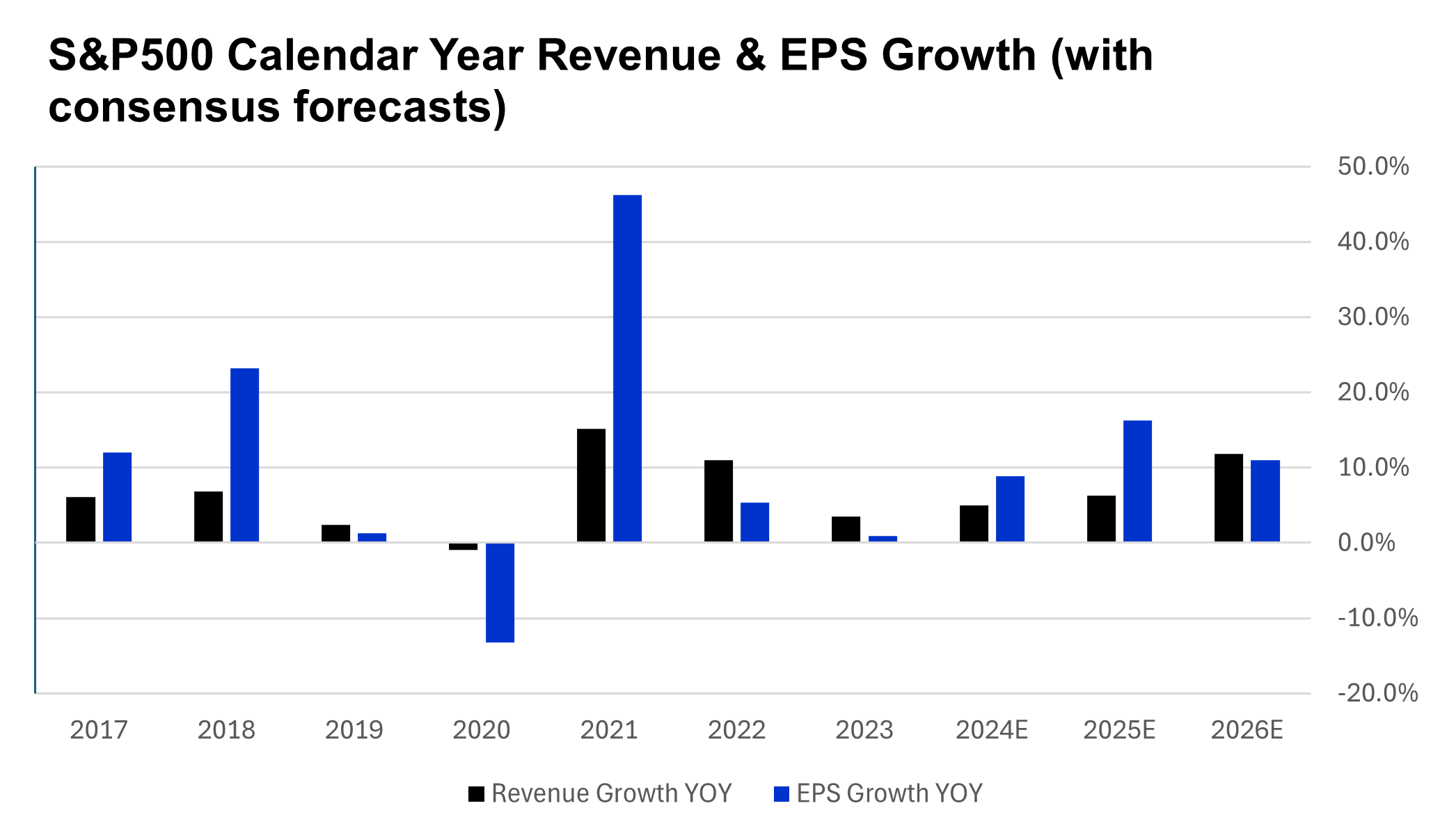

In addition to helping support the robust market performance over the past year, we believe this earnings season will be critical due to the aggressive assumptions that are baked into 2025 estimates. Despite a recent slowdown in economic activity, earnings estimates for 2025 have trended higher over the past year, with consensus bottom-up EPS estimates now standing at $275 (down slightly from a peak of $277 in August), which would imply 13% YoY growth. Within this forecast is an assumption that we will see 120bps of operating margin expansion for the overall index in 2025, with consensus expectations of a record 16.8% operating margins. This level is over 100bps higher than the prior record operating margin posted in 2021 (a year that saw 15% revenue growth and a 7% increase in inflation, which provided the cover for many companies to raise prices).

This quarter’s results and guidance will certainly provide insight into the ability of companies to meet these lofty assumptions, and any potential weakness could throw cold water on the recent optimism priced into the market, making these forward estimates seem further out of reach.

Third Quarter Index Level Expectations & Trends

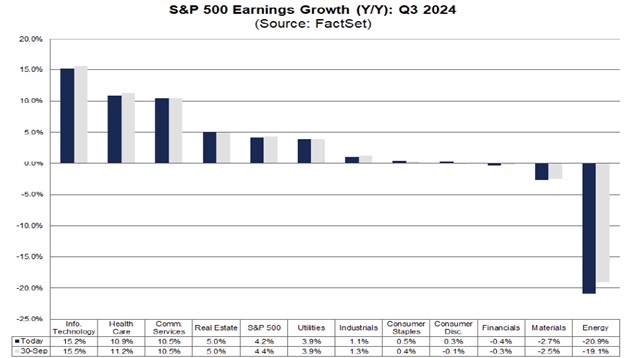

For Q3 2024, the estimated YoY EPS growth rate for the S&P500 stands at 4.2%, and while this would mark our 5th straight quarter of positive EPS growth, it is a substantial slowdown from the 13% YoY EPS growth we saw in Q2. Further, this measly 4.2% is about half the level of underlying growth analysts expected just three months ago.

While these negative revisions do set a lower bar for earnings beats, they ultimately reflect softer economic activity, and while GDP estimates have recently ticked higher, the reality is that profit growth remains somewhat elusive.

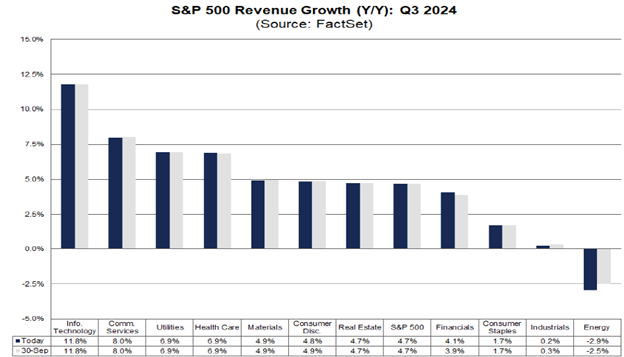

In terms of revenues, consensus estimates stand at 4.7% growth YoY. This is a slight downshift from the second quarter’s 5% YoY growth, but it is in line with the average revenue growth rate over the last several quarters, and broadly corporate revenues continue to track U.S. nominal GDP growth.

Turning to profitability metrics, consensus expectations are for a 410bps increase in index-level gross margins and an 80bps increase in index-level operating margins YoY. If these estimates are achieved in Q3, it would mark the best quarter of YoY margin expansion in three years and certainly set a positive tone for 2025.

In our view, this increase in overall corporate profitability illustrates the skill of many corporate management teams. These leadership teams remain adept at passing on modest price increases and effectively managing input costs, despite falling inflation and more price-conscious consumers. At the same time, the disconnect between gross and operating margin expansion illustrates how a tight labor market and payroll expenses, often the largest operational expense for a company, remain a substantial headwind to overall profitability.

Sector Trends Under the Surface

At the sector level, 8 of 11 sectors are expected to report positive YoY earnings growth, led by double-digit EPS growth in the Technology, Health Care, and Communications sectors.

Within the technology sector, the semiconductor industry is expected to post the strongest absolute YoY growth at +32%, as these companies continue to benefit from robust demand for the chips and equipment used in advanced computing.

The continued momentum in Technology sector EPS growth is contrasted by weakness in the more economically sensitive Energy sector, which continues to weigh on index-level growth and is by far the most profit-challenged sector in the S&P500. The Energy sector is expected to post an earnings decline of -21%, which would be the 5th YoY decline in the last six quarters, mainly a result of lower average selling prices for oil products and elevated production costs.

In terms of revenues, overall growth continues to be modest but broad-based. 10 of 11 sectors are expected to post positive YoY top-line growth, led by Technology, Communications, and Utilities. All three sectors are expected to post a sequential acceleration in revenue growth, and while it is unique to see this combination of sectors produce index-leading growth at the same time, the common theme for all three has been the relentless demand for AI technology and infrastructure, and recently, the increased demand for energy required to power this secular theme.

The Great Expectations for 2025

As discussed, expectations for 13% YoY EPS growth in 2025 are lofty in any year, but especially in an environment of slowing nominal GDP growth, which is the result of both moderating inflation and slower real growth. The last time we saw double-digit calendar year earnings growth was in 2021, a year that was boosted by 15% revenue growth, healthy fiscal stimulus, and accommodative monetary policy. 2021 was also a recovery year for earning as the -13% EPS decline in 2020 provided easier YoY comparisons.

While lower interest rates and slower labor cost growth should be positive contributors to earnings growth in 2025, it’s clear a heavy focus on profitability will be required for these expectations to be realized. Current 2025 consensus calls for record full-year operating margins of 16.8% (a 110bps increase off of what are likely to be already record-high margins in 2024). To get this degree of margin expansion in 2025, we will need to see further easing in the labor market and generally more operational efficiency across the board.

Ultimately, there is a narrow but possibly achievable path to double-digit EPS growth in 2025, which will require a combination of favorable macro conditions and skilled corporate management teams. At the company level, we will need to see continued gains in operational efficiency, productivity, and effective pricing. At the macro level, we will need to see the labor market continue to ease but walk the fine line of not overheating (increasing labor costs and pressuring margins) and not cooling so much that it weighs on overall consumption, the biggest driver of overall economic growth.

In our view, there are substantial risks to these 2025 expectations, and we believe earnings estimates will need to move lower, continuing a trend we have seen in recent weeks. This precarious environment of elevated valuations and negative earnings revisions requires investors to be mindful of risks, which means maintaining a valuation-disciplined approach, harnessing the benefits of diversification, and overall prioritizing quality businesses with management teams that are adept at generating operational efficiency and underlying earnings growth.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2024 NewEdge Capital Group, LLC