Click Here to Listen to the Audio Version

Introduction

“Gentlemen, you can’t fight in here. This is the war room!”

2026 was already shaping up to be an “interesting” year for markets, but the events of the past week have scrambled the outlook even further. What began as U.S and Israeli attacks on Iran have escalated into a wider regional conflict, significantly disrupting the flow of energy commodities out of the Persian Gulf and creating a reaction in just about every major financial market.

For now, the impact is most obvious in the spike in global commodity prices, while U.S. growth stocks have been remarkable resilient. Geopolitical risk only tends to have a large and lasting impact when it is a) severe; and b) prolonged. We will use this piece to detail the market reaction so far and the likely knock-on risks should the conflict last much longer.

Perhaps no piece of pop culture captured the uncertainty – and often the absurdity – of war planning more than Stanley Kubrick’s 1964 masterpiece, “Dr. Strangelove”. The gifted Peter Sellers inhabits a wide range of roles in the film, which parodies the darkest of topics: the prospect of nuclear war. We’ll be using some of the script’s memorable quotations this week to walk our readers through the market’s response to the current war in the Middle East and how a prolonged conflict might present further risks.

Where Are We Seeing a Reaction?

“Well, I would hate to have to decide who stays up and who goes down.”

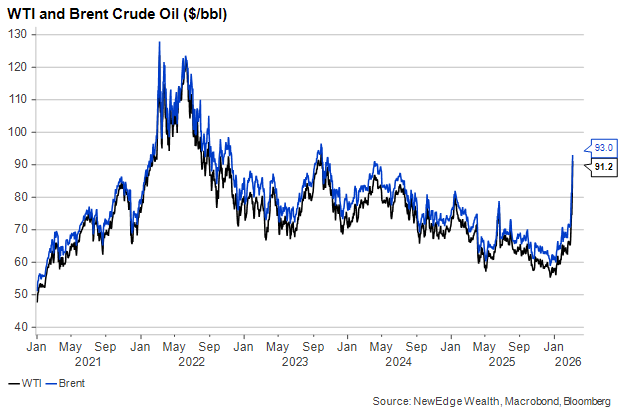

The Middle East has long been a hotspot for regional conflict, and given its importance to global energy output, investors always pay attention when a new war starts. The move we have seen in global oil prices over the past week is significant, the largest in the last three years. It is still dwarfed by the cumulative rise during the advent of the Russia-Ukraine war in 2022, as seen in the chart below, but the key question is if this jump higher in crude is just beginning and can be sustained.

WTI is a US-based crude price, while Brent is a Europe-based crude price and the better benchmark for what is produced in the Persian Gulf region. The spread between the two often indicates concern about supply disruption emanating from the war. In an understatement illustrated by tanker tracker videos, it has been more difficult for oil tankers to move in and out of the region, threatening the economies of Europe and Asia, which depend on oil and gas imports.

The strong rise in the U.S. dollar – unusual for periods of sharply rising commodity prices – means the energy burden in local currencies for most of these economies is even greater. Conversely, a rising dollar takes some of the sting out of this energy price spike for U.S. consumers and businesses.

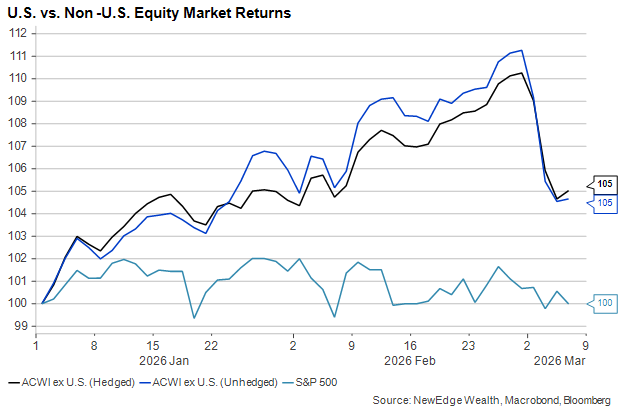

From an equity market perspective, the U.S. has endured the past week relatively well, while fears of economic pain – along with abrupt deleveraging-fueled selloffs in markets like Korea’s (“What, you don’t think I’d go into combat with loose change in my pocket, do you?”) – have caused non-U.S. markets to cede much of their outperformance from the first two months of the year.

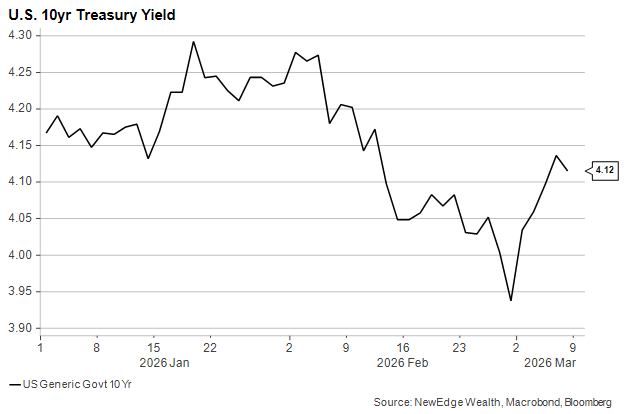

It feels like a long time ago when the U.S. 10-year Treasury yield dipped below 4% on a mix of A.I. optimism and labor market concerns. But a quick check of the calendar reveals that the 3.94% low only occurred on February 27th:

As the graph shows, things have changed thanks to the war in Iran. Markets now anticipate a hotter mix of growth and inflation will make it more difficult for central banks to cut rates. We’ll have more on the implications in our conclusion to this piece.

Where Are We Not Seeing a Reaction…and Why?

“Of course it’s a friendly call. Listen, if it wasn’t friendly, you probably wouldn’t have even got it.”

Going back more than fifty years, events in the Middle East have affected the U.S. economy and markets primarily through oil prices. As the U.S. has become a far larger energy producer, the impact from incremental flare ups has greatly diminished, to the point now where investors tend to ignore even the more serious risks.

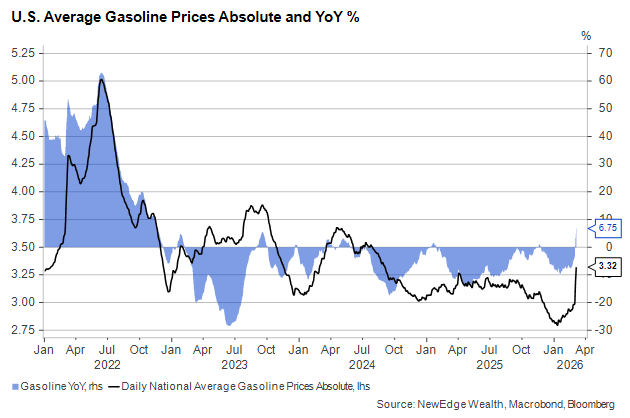

To wit, U.S. equity and credit market have acted as a bulwark against Iran-related risk, at least in the opening days of this war. We agree that the transmission from the conflict as it currently stands to the bottom lines of U.S. companies and consumer balance sheets should be limited provided oil prices come back down in relatively short order. Gasoline prices have risen high enough to be somewhere between a nuisance and a burden for U.S. households, but they have not been at these levels long enough to significantly impact the economy by forcing households to spend less in other areas:

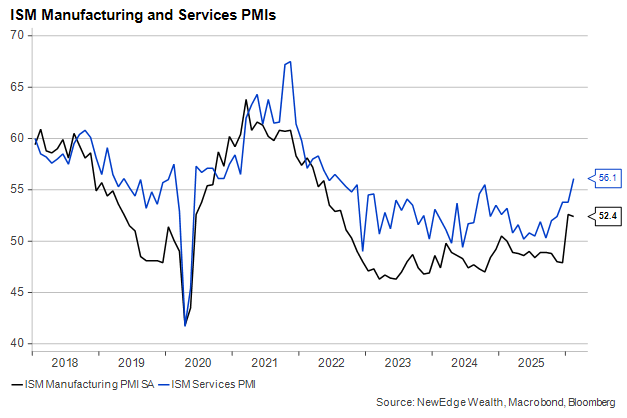

In addition, as the war headlines are spooking global markets, the U.S. has generally been getting better news on the domestic front. Both February ISM purchasing manager surveys – covering manufacturing and services – came in well above expectations and have shown a burst of life in the opening two months of 2026. While not perfect, these indicators rarely show acceleration without something good happening in the underlying economy.

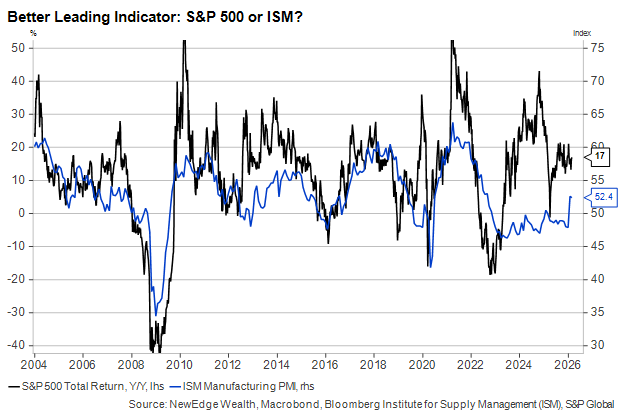

Whenever we mention the ISM these days, we must stress that the Manufacturing survey had until recently been in contraction mode over a three-year period that boasted above-trend growth. Still, despite their divergence in the 2020s, the ISM and the S&P 500 tend to move in tandem, as both are considered reliable leading indicators for the economy.

Here, the logic of U.S. equity resilience becomes somewhat circular. A prolonged conflict that creates a durable negative supply shock could eventually cause stocks to sell off 5 to 10% or more. But keeping stocks supported is, as we have written often in this space, one of the key goals for the Trump administration (“It is not only possible. It is essential!”) as it seeks to avoid an economic downturn that would further damage its midterm election prospects.

So, while a wider and longer war would eventually threaten earnings and valuations, investors know that the U.S. is likely to scale back from the conflict and seek a resolution if markets show significant signs of stress. This is precisely what occurred last April following the reaction to the announced set of so-called Liberation Day tariffs.

For the time being, WTI Crude oil at $90/bbl is an annoying but manageable level for the U.S. economy, creating a narrower set of winners (the large U.S. energy sector) than losers (households and other businesses). But should it persist, a lot of areas of the market that have, thus far, stayed quiet could start to make noise. We’ll conclude our piece by detailing those risks.

Conclusion: What Are the Risks to a More Prolonged Conflict?

“Well, uh, I’d like to hold off judgement on a thing like that, sir, until all the facts are in.”

A durable rise in commodity prices creates higher headline inflation and lowers consumer purchasing power. This occurred in both the mid-2000s with the commodity price spike that preceded the financial crisis and in 2022 when oil and gas prices shot up after Russia’s invasion of Ukraine.

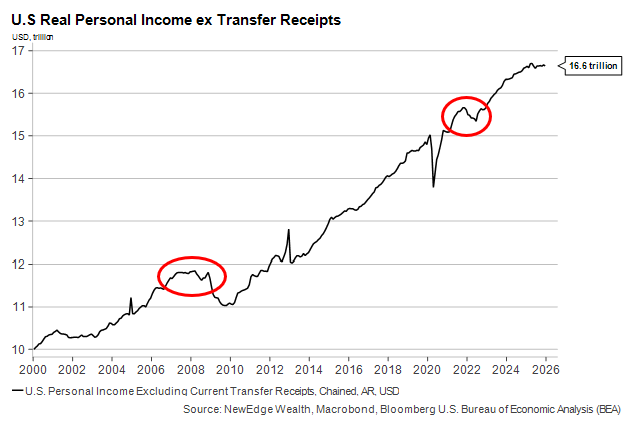

Both periods are noted with red circles on this graph. The 2008 example, in which savings rates were low and household balance sheets were stretched, obviously ended in recession (not primarily because of the commodity price impact, we should note). The 2022 example, in which consumers came into the spike in far better shape, did not. Personal savings rates today are as low as they’ve been outside of 2021 (when stockpiles of savings were still massive) and the mid-2000s.

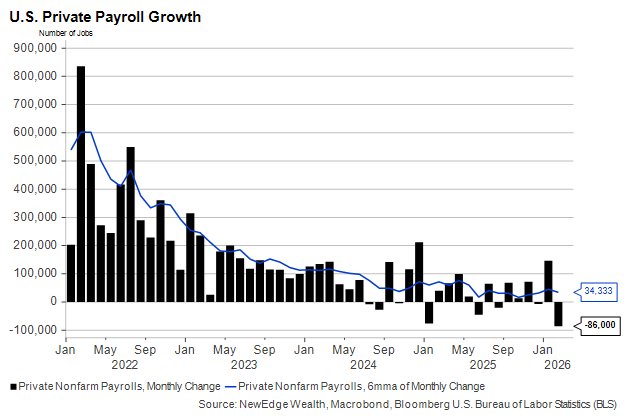

As the end of the chart above shows, real incomes have already been flat for close to a year despite what had been a gentle decline in energy costs. That’s been partly due to the weaker labor market, which, as February’s U.S. employment report showed, is seeing unemployment rise as job creation all but vanishes. Add higher prices on a mandatory item like gasoline into the mix, and we could start to see larger cracks forming in the U.S. consumer.

The Fed could eventually feel pressure to ease monetary policy with lower interest rates, despite inflation moving even further away from its target. Central bankers can’t do much about a negative supply shock (e.g., rising oil prices) other than create a negative demand shock to offset it. This outcome is rarely desirable. But given the Fed’s political mandate to lower rates and stimulate the housing and manufacturing sectors, energy price inflation that leaks down (via fuel costs) into core areas like transportation is a problem.

We will be updating our readers regularly should developments in the Middle East significantly alter our outlook or our investment approach.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC

The post How Investors Learned to Stop Worrying and (Mostly) Shrug Off Geopolitical Risk appeared first on NewEdge Wealth.