“It started out like a song.”

Something is stirring. Shifting ground. It’s just begun. This month, investors seem to have finally cast aside their inflation worries as they focus more on risks to global growth. Commodities prices have plunged, bonds are rallying, and central banks are cutting interest rates.

As a result, the rules of portfolio diversification are changing again. Navigating the ongoing slowdown may require investors to unlearn some of the painful lessons of 2022 and 2023. Luckily, we have Steven Sondheim’s lyrics (from the Tony Award-winning musical “Merrily We Roll Along”) to help explain it all.

“Time goes by, everything else keeps changing.” With inflation licked, markets have moved on to growth concerns.

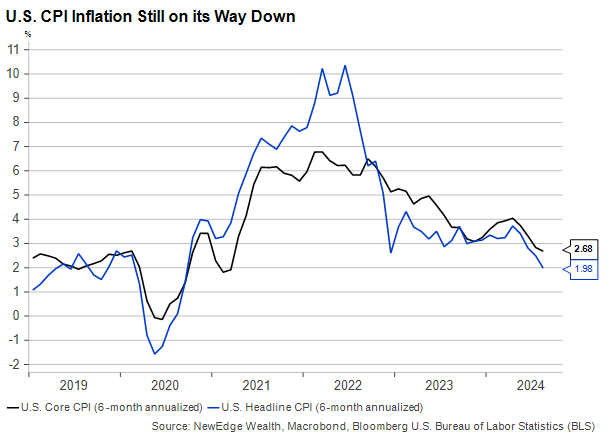

Noisy, lagging and partly fictitious shelter costs aside, inflation is no longer high in the U.S.

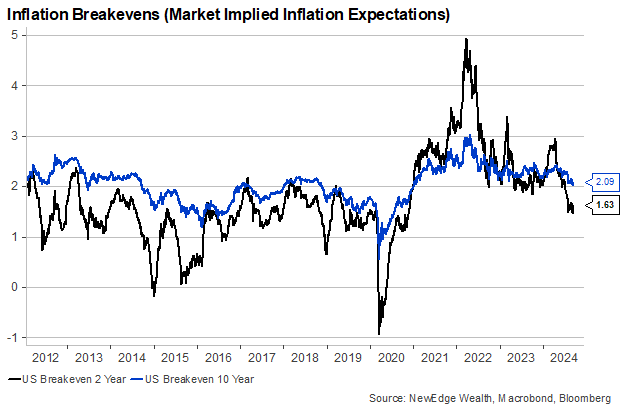

Over the past six months, headline inflation has fallen to a 2% rate, but excluding shelter, the figure is just 0.5% thanks to falling durable goods and energy prices. As the inflation tide has moved out, market-based measures like TIPS inflation breakevens, and survey-based measures like the one in the University of Michigan Consumer inflation poll have followed.

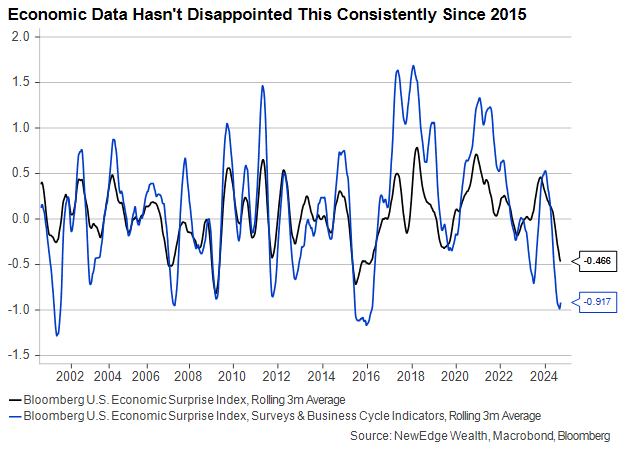

Meanwhile, growth data has been more likely to fall short of expectations than at any time in nearly a decade, according to the Bloomberg Economic Surprise Index. The softening labor market is getting most of the attention, but survey-based measures of the economy, which tend to be the best leading indicators, account for the lion’s share of the disappointment. Just this week, we learned the apparent burst of small business confidence in the July NFIB survey reversed – and then some – in August.

The combination of strong growth and hot inflation had a huge influence on financial market behavior in recent years. But now cooler conditions are rolling in, and the environment looks more like it did in the mid- to late 2010s. We see several ways in which portfolio strategy needs to change to adapt.

“How did you get to be here?” What drove correlations crazy in 2022?

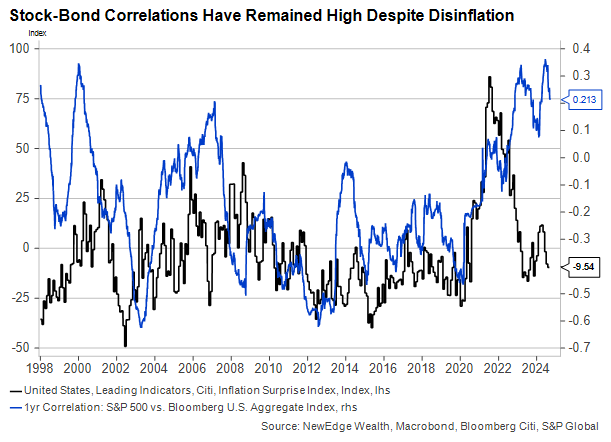

We can’t recall a reversal in cross-asset correlation quite as jarring as the one that began in late 2021. Correlations between stock and bond prices just about everywhere in the world swung from negative to positive in the blink of an eye, sending portfolio volatility higher and investor funds into cash. But we are just now starting to see signs that they’re swinging back.

Investors have been told for decades to own a mix of asset classes – chiefly stocks and bonds, for most – to achieve higher risk-adjusted returns. For that to work, bonds and stocks must be uncorrelated, preferably negatively correlated.

Recent history tells us that high inflation is the enemy of diversification. As inflation outpaced just about every economic forecast in 2021 and 2022, it became the main driver of interest rates. Higher inflation and the policy response they invite were rightly seen as obstacles to future economic growth and dimmed prospects for assets (like stocks) correlated to it.

The week’s data notwithstanding, inflation has generally fallen faster than expected from the 2022 peak. Despite this, the correlation between stocks and bonds has been slow to revert to its strongly negative range from the 2010s. But it may be just a matter of time. Stocks and bonds have been most negatively correlated during a) recessions; and b) prolonged periods of tame inflation.

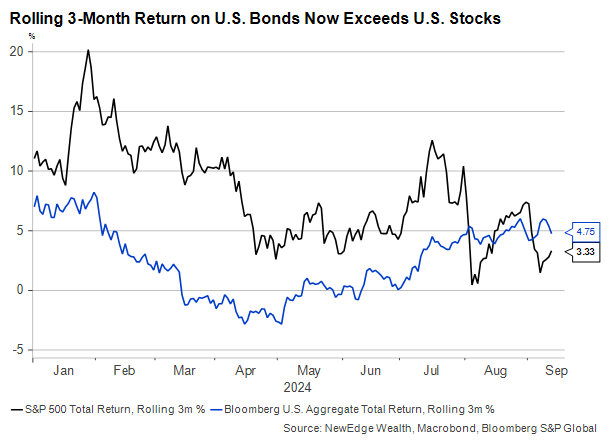

“We had a good thing going.” Slower growth helps bonds and hurts stocks.

Investors should feel fortunate that the benefits of diversification seem to be returning just as the stock market rally has begun to lose some steam. Bonds have just staged their best three-month period of 2024 while the S&P 500 is having one of its worst. It’s unusual for bond returns to beat stock returns, even for short periods, when returns on both asset classes are positive. But that’s just what happened this summer.

“Still with dreams. Just reshaping them.” What assets perform well in slowing growth environments?

It’s all well and good to point out that diversified portfolios are coming back into fashion as growth slows and inflation normalizes. But drilling down into individual asset classes, what can we say about how individual factors behave in such an environment?

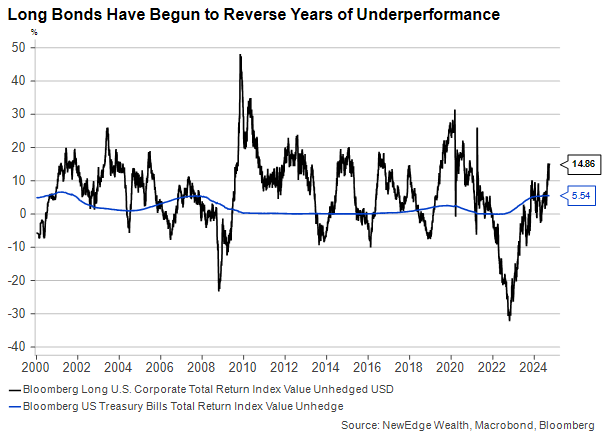

It may be easiest to start with fixed income, where investors have been rewarded for huddling in cash and other short-duration instruments given the yield curve has been inverted and the longer end has been subject to so much volatility. But those years of short-duration dominance are likely over.

Longer-duration investment grade corporate bonds are finally beginning to claw back their underperformance against Treasury bills, as they typically do when the Fed is cutting rates and/or economic growth is slowing. If we have a single high conviction view about 2025, it’s that the returns on cash will be measurably lower than they were in 2024.

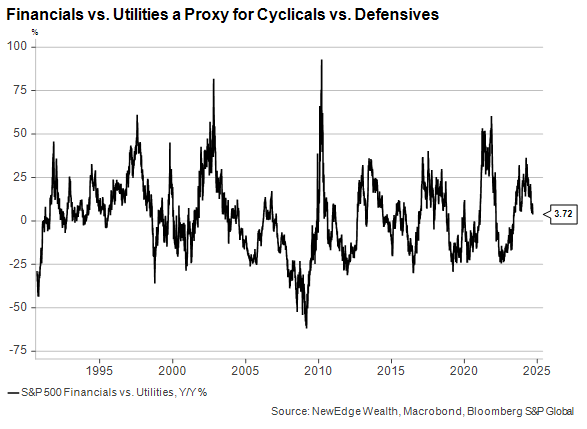

Things are less clear cut in the equity market, where leadership has been shifting day to day depending on the market’s mood. With corporate earnings season behind us, investors must rely more on “vibes” for the next few months. With economic data generally coming in softer than expected, defensive segments of the market have started to perform better.

Compared to cyclicals, defensives offer more stable earnings growth and generally pay higher dividends. This makes their performance correlated to the returns on bonds against stocks, and that relationship is holding up in the second half of 2024 thus far.

Technical signals tell us that the rush into Utilities and other defensive sectors may be overdone for now, but their performance from here will continue to hinge on the weakening growth outlook and the speed with which the Fed reduces its target interest rate.

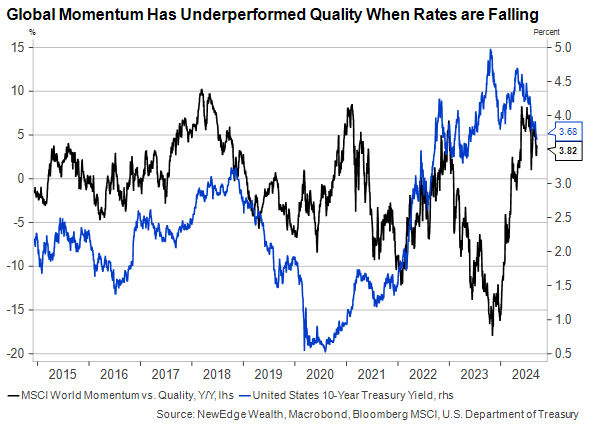

Looking at individual equity factors, we’ve noted the recent struggles in high momentum stocks after a torrid run during the first half of the year. Here, we compare them to the Quality factor, which captures companies with stable earnings growth and healthy balance sheets.

Interest rates are far from the only factor that drives the performance of these two market factors over time, but periods of falling rates have been associated with quality outperformance against momentum. Downward inflection points in the economy or interest rates tend to be the enemy of momentum.

“I miss it. And I want it back.” Conclusion.

For those who haven’t seen it, Merrily We Roll Along is a tragedy told backwards. This causes the hopeful finale of the play to land bitterly, because the audience knows about all the unpleasantness to come. We don’t have the power to follow economic and market developments in reverse, but we know the start of the story for bonds and diversified portfolios since the start of Fed hiking was far from happy.

Whether the economy lands softly or not in 2025, the prospect for fixed income has improved on just about every dimension, from valuation to policy support. Bond investors can finally sing “our time” and be confident they’re right.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2024 NewEdge Capital Group, LLC