“Burnin’ out of control…” – Inflation Data Sets a New Tone for Bond Markets

It’s never fun to write about disappointment on Valentine’s Day, but Pat Benatar would agree that this week’s inflation data was more “love taker” than “dream maker”. The January U.S. Consumer Price Index (CPI) inflation report data showed the past two years of goods price deflation winding down while “core” services prices like airfares and care insurance premiums remain on the rise. The sharpest one-month rise in egg prices since 2015 was the last pinch of salt in the wound (small consolation: salt prices remain flat year on year).

This inflation report likely slammed the door on any further rate cuts from the Fed for now, making it a “Heartbreaker” for consumers, businesses, and investors who had hoped for help from easier borrowing conditions in 2025. For reasons we’ll cover in this report, our outlook for rates to stay high does not rest solely on this week’s upside inflation surprise.

We do not see rates falling much in 2025 absent a growth scare. This could prove challenging for segments of the economy that were counting on lower rates, as well as for investors expecting better returns on their bond portfolios. In the latter’s case, we continue to see bonds as an important diversifier against an economic slowdown and a reliable source of income.

“Drownin’ me in your promises…” – Rates Aren’t Going Down

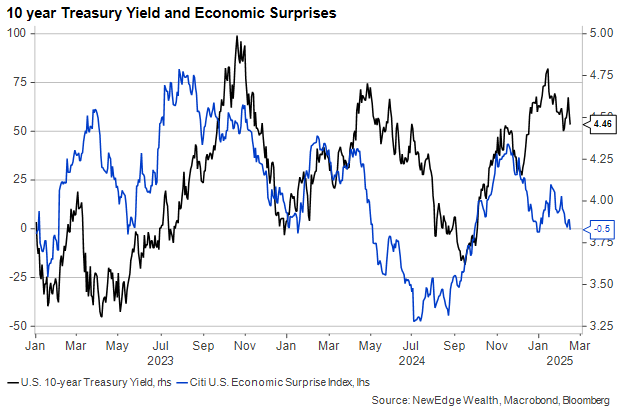

About six weeks into 2025, it still looked like interest rate risk (i.e., bond duration) could be a tailwind for diversified portfolios with the Fed still hanging onto an easing bias and growth data looking ho-hum. By the opening days of February, the 10-year U.S. Treasury had fallen by 16 basis points from its end-2024 level, with the low coming on the heels of a soft ISM Services business sentiment survey.

But this past week included a slew of new announced taxes on U.S. imports, an upside CPI surprise and a proposal for around $3.3 trillion (give or take) of additional borrowing in the Congressional budget over the next ten years. Collectively, these sent the 10-year yield as high as 4.65% before softness in a few key January Producer Price Inflation categories allowed yields to ease back down.

The drivers that have sent rates higher over the past few months, and more specifically this week, seem likely to us to remain in place for now. We know a little more about coming fiscal policy changes than we did a week ago, and it seems clear that deficit reduction, which could have helped reduce long-term rates, is not in the cards (the cuts by DOGE certainly make headlines, but they are barely scratching the surface of the kind of spending cuts that would be needed to significantly alter the deficit trajectory). Tariffs – or, at least, tariff announcements – continue to roll out, which could boost goods prices almost immediately, adding to the backdrop of sticky inflation and thus higher-for-longer rates.

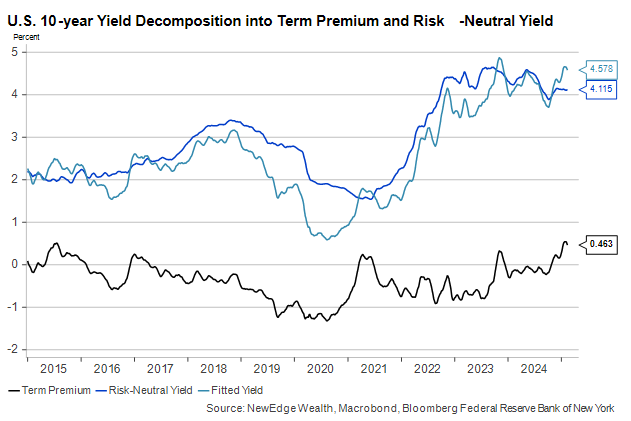

When we decompose the 10-year U.S. Treasury yield into a) expectations of future short-term rates; and b) the term premium (or Treasury risk premium), we can see that most of the recent rise has come from the latter. Holding Treasuries over the long term has become a riskier bet, or, at least, one that investors are demanding to be better compensated for making.

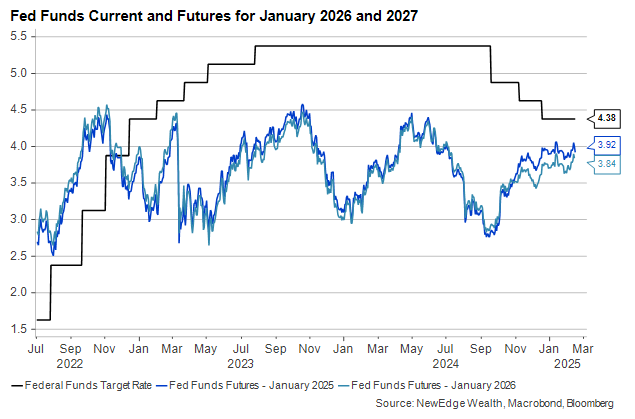

The Fed’s open market committee (FOMC) appears set to keep policy on hold for the time being, compared to just a few months ago when both investors and the FOMC itself saw scope for further rate cuts in 2025.

Dallas Fed President Lorie Logan signaled a change to the Fed’s reaction function when she said last week, “What if inflation comes in close to 2 percent in coming months? While that would be good news, it wouldn’t necessarily allow the FOMC to cut rates soon, in my view.”

Logan and her colleagues will need to see rising unemployment and falling inflation to feel further cuts were appropriate. The bar to policy easing, in other words, has been raised (though we would note that the bar to raise rates further is also high, suggesting a “hold” stance by the Fed).

“Now it’s takin’ its toll…” – Heartbreaking Economic Implications

If interest rates do not fall in the medium term, there could be implications for both the economy and the markets. Consumers have been unexpectedly resilient to high rates over the past three years, due partly to the hot labor market and partly to rising stock prices and home equity.

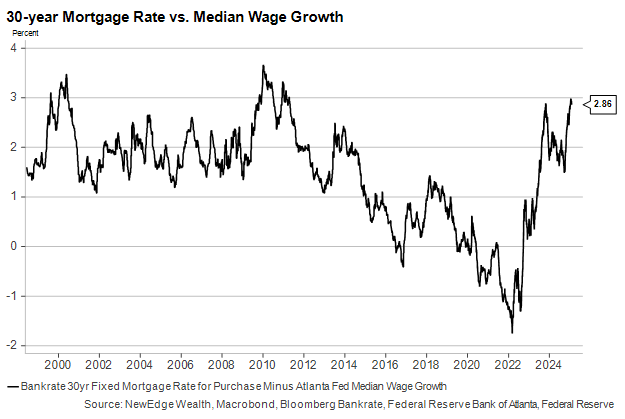

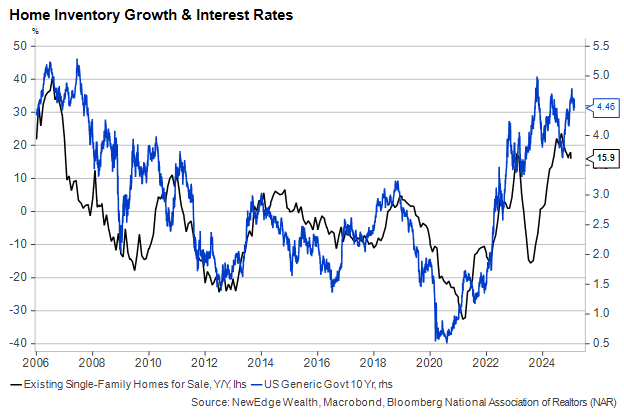

However, strains on the consumer may be emerging. Median wage growth has fallen to its slowest pace since 2021, while the cost of financing a new home has risen. This should continue to cause home sales to slow in the opening months of 2025.

Home buyers are scarce with rates at these levels, which is why higher levels of the 10-year U.S. Treasury yield are associated with more rapid growth in homes available for sale. This could discourage new projects (housing starts are already low) and threaten what to this point has been remarkably resilient demand for labor in the construction sector.

Weak sales and starts have not yet weighed on home prices, but that moment could be coming if rates stay high and inventories continue to pile up. This along with equity market volatility is one of the chief threats to continued consumer spending growth, much of which has been driven at the high end by the wealth effect.

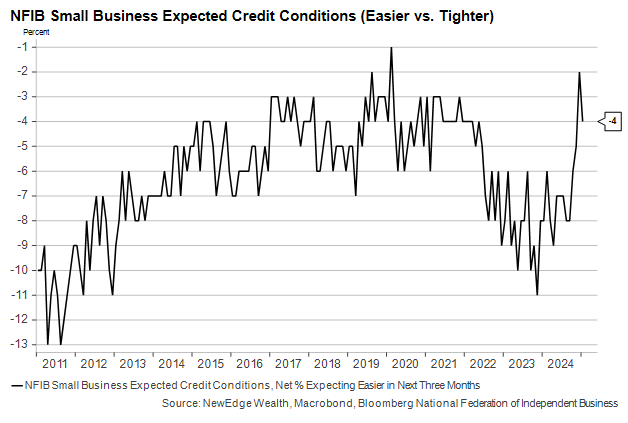

The toll that high rates take on small businesses was probably the main reason the Fed elected to cut interest rates starting in September of last year. At the time, surveys of business owners were in the doldrums, but these surveys have turned higher following the Fed’s 100 bps of rate cuts and the November U.S. election results. Underpinning that confidence is a more widespread belief (as exhibited in the NFIB Small Business Survey) that credit conditions will improve in the next six months. If that doesn’t pan out, companies that were expecting to be able to borrow more cheaply or refinance at lower rates may find their plans to hire or invest derailed.

“And you know that you were born to be…”– Implications for Fixed Income Investing

Fixed income investors have not had much to be excited about over the past three years, but the bond rally last summer carried some hope of a return to the forty-year period that preceded the pandemic: a long march lower for inflation and interest rates. But for the reasons outlined above, we cannot be as optimistic that the next few years will see bond yields fall consistently.

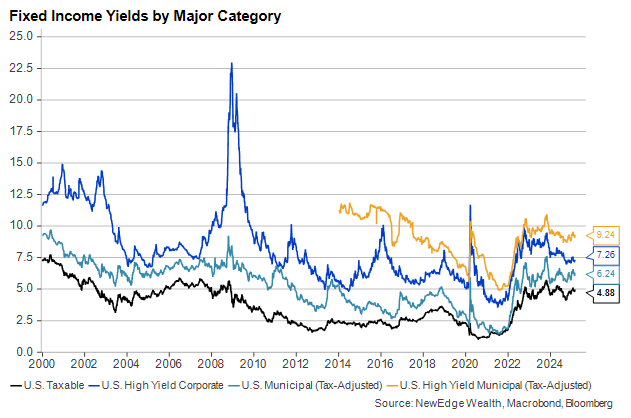

Investors should become accustomed to “clipping coupons” on most types of bonds for the time being as income, not price appreciation, becomes the dominant driver of total returns. The good news is that those coupons are larger than they’ve been for many years, especially those on municipal bonds once we consider the benefit of their tax-exempt status.

Coming into the year, our expectation was for a wide and choppy range for long-term rates. Should the 10-year Treasury rise to a much higher level (say, 5% or higher) we would be more tempted to hold longer duration positions. Currently, however, we are dually cautious about both credit and interest rate risk. Spreads on corporate bond yields above Treasuries remain tight, and the Treasury yield curve (despite the higher term premium) remains relatively flat. We prefer opportunities in municipals (taxable and non-taxable) and certain lagging segments of structured credit, including non-Agency MBS.

“Don’t you mess around with me…” – Conclusion

Six months ago, markets were behaving as if the inflation wind that first hit us in 2022 was dying down and the return to a bond bull market was imminent. Central banks seemed to be encouraging that view. But events since then should lead investors to lower their expectations somewhat for what fixed income returns will be in 2025. Acute risk aversion – stemming from a recession that just never seems to get here – would be the clearest catalyst for lower interest rates and better bond returns. Those still singed by the memory of synchronous stock-bond losses in 2022 should recall how well bonds performed in previous slowdowns like 2008. While few are rooting for such an outcome, there are a limited number of asset classes that would perform well should it pan out. High-quality bonds are one of them.

To those with Valentine’s Day plan over the weekend, we hope your dinner dates exceed expectations by as much or more than fixed income returns have missed them.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2025 NewEdge Capital Group, LLC

The post Heartbreaker appeared first on NewEdge Wealth.