Anywhere you go, I’ll follow you down

I’ll follow you down, but not that far

“Follow you Down”, Gin Blossoms

Splintering of relationships is common, if not expected, in rock band lore. Some schisms prove temporary and seem to heal with time (and money… like Oasis), some appear more lasting (like Rage), and some are tragically permanent (like the original lineup of the Gin Blossoms).

Currently, there is a splintering in financial markets and economic data that is likely to prove temporary, but as this splintering mends, markets could be singing Gin Blossoms’ “Follow You Down” along the way.

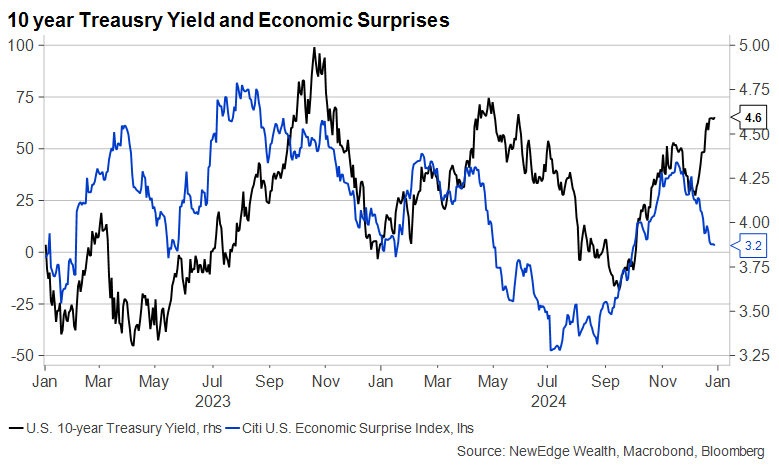

“I Know We’re Headed Somewhere, I Can See How Far We’ve Come”: The Divergence of Yields and Economic Surprises

Over the past few years, there has been a strong relationship between the 10 Year Treasury yield and economic surprises.

When economic surprises are moving higher (data is beating forecasts) we have seen the 10 Year yield rise, but when economic surprises are moving lower (data is missing forecasts) we have seen the 10 Year yield fall.

Economic Surprises are a measure of how economic data is coming in compared to expectations, with a positive and rising Economic Surprise Index reflecting economic data beating consensus forecasts, and a negative and falling Economic Surprise Index reflecting economic data missing consensus forecasts. When Economic Surprises are positive/moving higher it suggests that analysts may need to raise growth forecasts and if they are negative/moving lower it suggests that analysts may need to cut growth forecasts.

This makes sense intuitively: higher yields reflect both higher growth/inflation and reduced demand for safety assets like Treasuries, while lower yields reflect both lower growth /inflation and higher demand for safety assets.

However, over the last month, economic surprises and the 10 Year Treasury yield have splintered, just like a feuding rock band.

The chart below shows this divergence, with the 10 Year Treasury yield rising to around 4.60%, all the while economic surprises have plunged as economic data has surprised less to the upside and/or missed expectations.

As of 12-27-24

There have been multiple instances in recent years where this splintering has occurred, with economic data turning weaker while Treasury yields pushed higher, but in each of these instances it was Treasury yields that sang the Gin Blossoms, saying to economic surprises “anywhere you go, I’ll follow you down”.

One example is from 3Q23, when economic surprises began to turn lower in the summer, but Treasury yields pressed higher on increased issuance of longer-dated, coupon bonds by the Treasury. This caused the bond market to grow concerned with this increased supply, sending yields spiking to 5%. Eventually in early 4Q23, Treasury walked back its increased issuance and yields peaked, quickly following economic surprises down.

Another example is from earlier this year in 2Q24, when Treasury yields spiked higher in April, all the while economic data was softening and economic surprises were turning lower. Weaker data eventually caught up to Treasury yields, pulling them down through 3Q24. Economic data softened through the summer and contributed to the Fed’s hastened jumbo 50 bps interest rate cut in September.

Interestingly, economic data had been improving before the September cut (or maybe analysts had just cut their forecasts too much!), which then paired with the knee-jerk jumbo cut from the Fed in September, marked the low for yields. Since that September cut, the 10 Year has soared 100 bps, following economic surprises up, but also a notable splintering of the typical relationship between long yields and the start of Fed cutting cycles.

The conclusion from these past examples is that in the short run, other concerns can drive the 10 Year yield but over the medium term, 10 Year yields can’t outrun weaker economic data.

We think these “other concerns” driving the 10 Year higher today are a combination of Treasury deficit funding (in the run up to hitting the debt ceiling at the beginning of 2025, when the draining of the Treasury General Account could push yields lower), liquidity dynamics around tax payments (this is from Dan Clifton of Strategas’ great work showing that post large tax payments, such as this December’s, Treasury yields have tended to rise), inflation fears (following the revision higher of the Fed’s inflation expectations at last week’s Fed meeting), and shifts in Fed policy expectations (namely the constant creep higher of the long-run neutral rate forecast, which we think still has room to be revised higher).

But again, if economic data continues to come in below expectations, then these dynamics may eventually take a back seat.

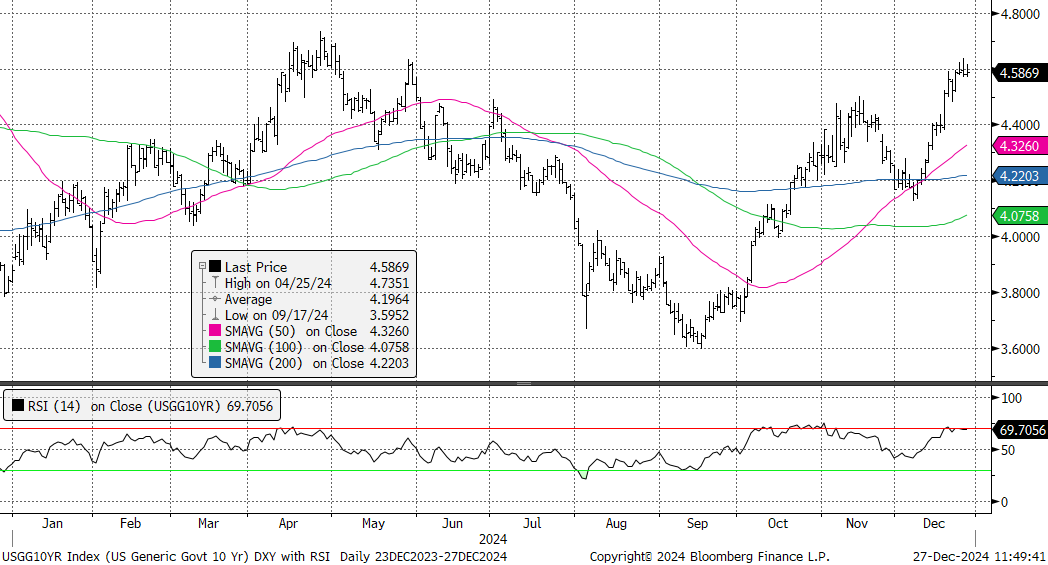

“How You Gonna Ever Find Your Place, Runnin’ at Artificial Pace?”: 10 Year Technicals

The 10 Year’s “December to Remember” pop higher has left the yield in a state where it is now technically overbought, as measured by the Relative Strength Index shown below, into some resistance around its highs of the 2024. A similar condition presented itself in October/November, before yields took a brief pause in their ascent (notably yields pressed higher in November even as momentum was fading, setting up for the pull back in yields later in the month).

The tactical conclusion here is that we may see yields take a breather lower when we begin 2025 given this technical setup.

U.S. 10 Year Treasury Yield and its Relative Strength Index

Source: Bloomberg, NewEdge Wealth, as of 12-27-24

We will be presenting our 2025 Outlook on January 15th (keep an eye out for the calendar invite!), with time devoted to our expectations for the medium term outlook for the 10 Year yield (spoiler alert: we see the wide, volatile range of 2024 persisting into 2025, so keep your seatbelts fastened!).

“Let’s Not Do the Wrong Thing and I Swear it Might Be Fun”: Conclusion

Overall, the combination of the technical setup for yields and the divergence between yields and economic surprises, suggest to us that in the very near term, yields could be biased lower. This could create a buying opportunity for fixed income (taxable and tax exempt) investors who are looking for opportunities to lock in higher yields and extend duration.

We see the yield volatility of 2024 persisting into 2025, but as we say within equity markets “volatility creates opportunity”, so the recent rise in yields, despite softer economic data, may just be presenting one of those opportunities.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2024 NewEdge Capital Group, LLC

The post Follow You Down appeared first on NewEdge Wealth.