Fear the light

Fear the breath

Fear the others for eternity

But I hear them now, inhale the clarity

“Fear Inoculum”, Tool

When after a thirteen-year hiatus, Tool released their fifth studio album, Fear Inoculum, the Internet was aflutter with potential meanings and interpretations of the much-anticipated release.

Theories about the meaning behind Maynard’s “allegorical elegy” ranged from confronting aging, to fears of failure after the hiatus, to spiritual descent and awakening, to time travel (!!). But one Fear Inoculum interpretation from a simple Redditor resonated most with us as we contemplate the state of markets and the economy: “get comfortable being uncomfortable.” This is a message of making the most of fear and making it work for you, a theme we will explore in this week’s Weekly Edge.

“Hear the Venom”: The DC Detox Key Change

We have been sharing this message of “get comfortable being uncomfortable” in talking about a lower return, higher volatility, wide/choppy range for equity markets in 2025. But in another way, we also note that this “get comfortable being uncomfortable” has been a key message coming out of the White House. President Trump and officials have been using words like “detox”, “disruption”, “transition period”, and even “pain” to describe the short-term challenges that they say will result in long-term gains.

This administration’s embracing of discomfort, a distinct key change from Trump 1.0’s “all I do is win” approach, has rattled markets that had so resolutely expected “just the right stuff” out of DC. We warned of this overly sanguine outlook for DC in our 2025 Outlook and again in early February, arguing that good things could certainly happen, but “Great Expectations” and high valuations left very little cushion to absorb bad news.

So, as U.S. equity markets have shuddered with negative news flow hitting lofty valuations, we have also seen fear amongst investors pick up meaningfully.

“Exhale, Expel, Recast My Tale”: The Role of Fear

Fear is a fascinating emotion when it comes to markets. Experienced on an individual level, fear can be a blinding and distorting emotion when making market decisions, but measured on an aggregate level, fear can be illuminating and insightful when making market decisions.

Said another way, as an individual, fear can lead to poor decisions (such as selling at market lows), but in aggregate, fear can be used to make great decisions (such as buying at market lows). When aggregate fear spikes and becomes the consensus emotion, history shows that contrarian optimism is often rewarded. Warren Buffet’s timeless aphorism is the framework: “Be fearful when others are greedy and greedy when others are fearful.”

This is why, in times of market duress, we spend copious time looking at different ways to measure investor fear in aggregate. The effort, in the words of Maynard, is to become “inoculated” to individual fear and “inhale the clarity” of aggregate fear.

“Venom in Mania”: Market Based Fear Assessments

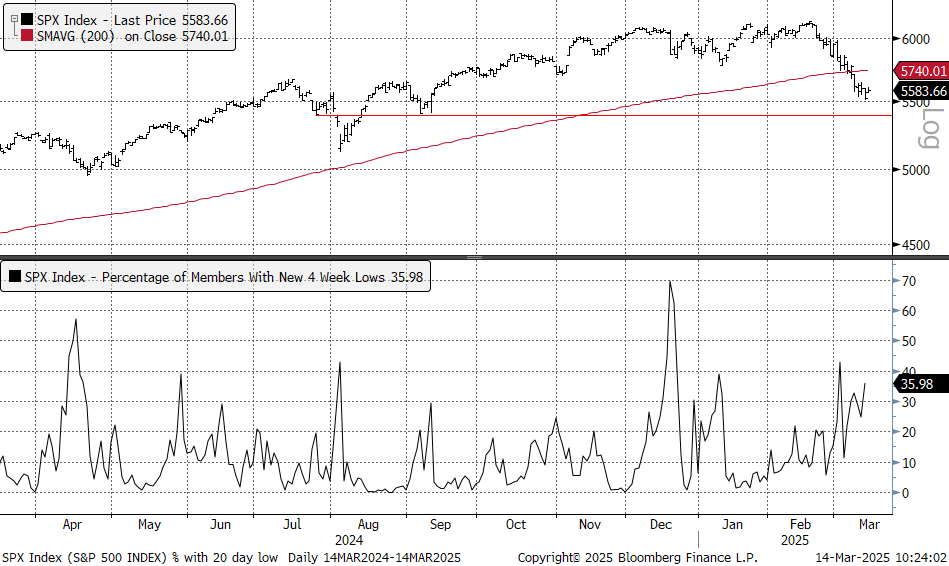

We begin our assessment of aggregate fear by looking at signs of indiscriminate selling in the market. When it appears that investors are “throwing the baby out with the bathwater” and selling all equities, despite their relative merit, it can be a sign of peak fear and capitulation in markets.

One way to measure this capitulation is by looking at the percentage of stocks in the S&P 500 making new 20-day lows. When this measure spikes above 50%, it is indicative of this indiscriminate selling that often marks market lows.

The chart below shows that as of the close on Thursday, this measure has reached 36%, below the typical “flush” threshold. This lower reading, despite the 10% decline in the S&P 500, can be explained by weakness being most pronounced in large weighted, high momentum Mag 7/tech/Growth stocks, along with the relative resilience in some defensive sectors.

S&P 500 with % of Members at New 20 Day Lows

Source: Bloomberg, NewEdge Wealth, as of 3-14-25

We can also measure indiscriminate selling through breadth measures like the percentage of names above their 50- and 200-day moving averages, which the chart below shows have deteriorated sharply in recent months but remain slightly above levels seen at major market lows (such as in 2022 or 2023).

S&P 500 with % of Members Above Their 50- and 200-Day Moving Averages

Source: Bloomberg, NewEdge Wealth, as of 3-14-25

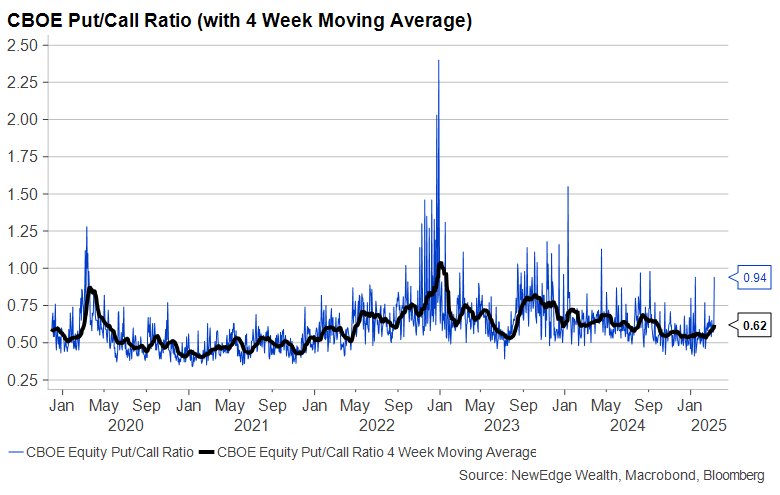

We can also measure fear by looking at investor demand for downside protection, which tends to spike when fear spikes. Flows into leveraged downside ETFs provide a window (these have not been substantial), or options activity, as we look for spike in the ratio of demand for downside protection with puts versus upside optionality with calls. This Put/Call ratio has jumped as of Thursday to well above the “complacent” levels we saw earlier this year when the market was at highs, however the ratio remains below prior peaks seen at prior major market lows.

As of: 3/14/25

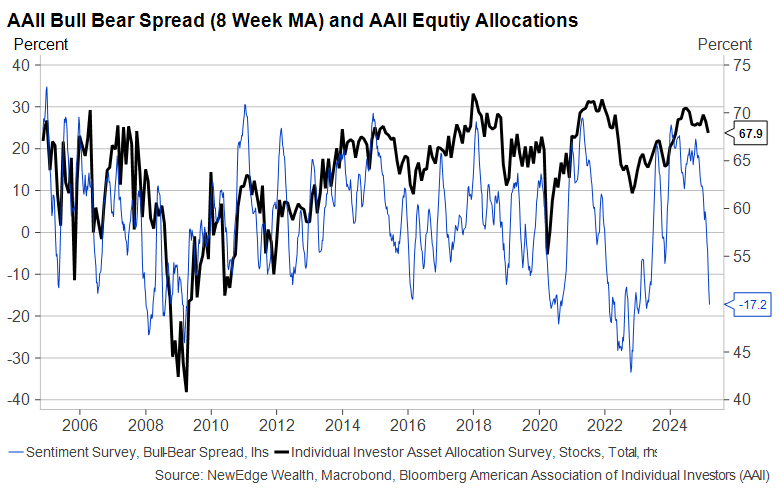

Lastly, we can also look at survey data of investors to see how fearful they say they are. Participants in the AAII sentiment survey are reporting a dominant bearish/fearful sentiment, but in a classic “watch what they do, not what they say”, we have yet to see this fear result in a meaningful reduction in equity allocations (seen below). Household allocations to equities remain near multi-decade highs (and all-time highs in the Fed’s Flow of Funds data), which is one reason that we flagged a negative feedback loop of weaker equities hitting the wealth effect and high income consumption as a key risk for U.S. economic growth in 2025.

As of: 3/14/25

Overall, these measures show that aggregate fear has increased substantially during this correction, but it is not at an extreme level that has been seen a major market lows. This does not mean that recent weakness does not provide investment opportunities for those sitting on large cash balances, but it does suggest that this bout of volatility and market chop we have been enduring could continue (even if we see a near term bounce off of oversold levels). And so we are reminded, as our Tool Redditor opined: “get comfortable being uncomfortable.”

Contagion I Exhale You: Growth Fears

We also have to consider aggregate fear in the forecasting of growth for earnings and the economy. When fears about growth spike and the “r-word” (recession) becomes increasingly used, investors must ask if forecasters have become too pessimistic about the forward prospects for growth.

We have certainly seen growth fears pick up in recent weeks, but to nowhere near the levels of “absolute-recession-certainty” that we saw during 2022’s bear market. We also began the year with such universal optimism about the U.S. economy (including Powell’s 5x adulation about how great the economy was in December’s Fed meeting!), that some reassessing of potential risks is normal.

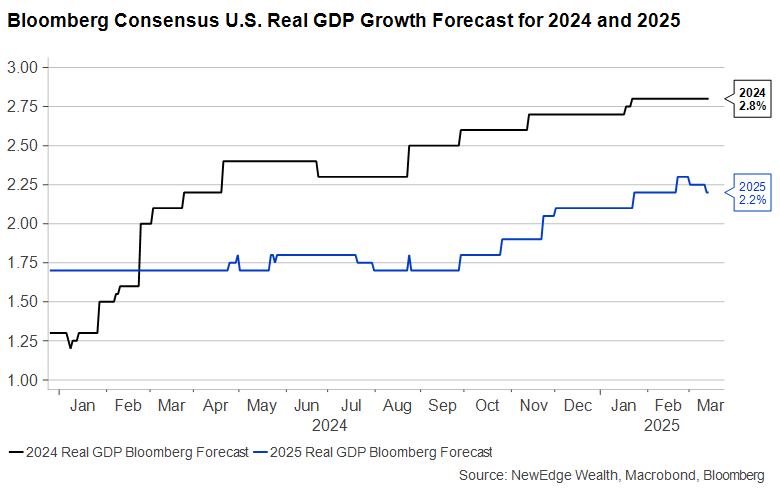

The chart below shows Bloomberg’s recession probability index, which has ticked higher for the first time since early 2023, while the second chart shows how 2025 GDP forecasts have started getting trimmed (with high profile cuts to forecasts from Citi, Goldman, and now JP Morgan).

As of: 3/14/25

As of: 3/14/25

Both of these revisions are a notable change from the falling recession/rising growth forecast trend over the last two years, which provided a strong backdrop for risk asset performance. If these revisions continue (rising recession /falling growth forecasts), we would expect a continued choppy environment for risk assets (equity and credit).

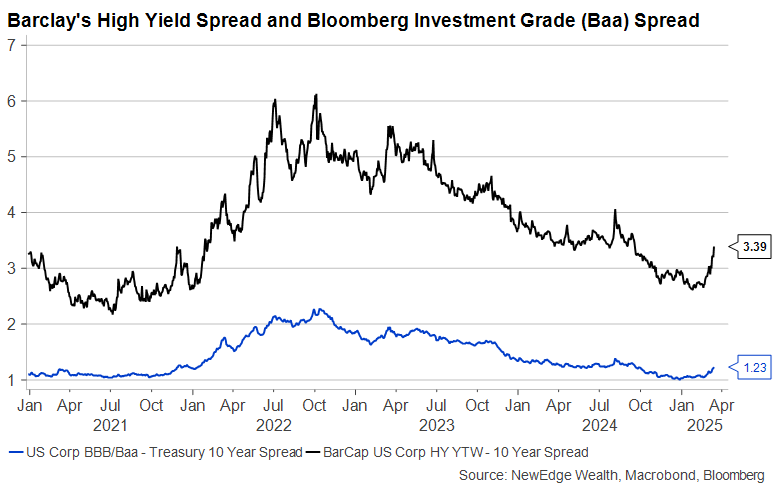

On credit, we also must monitor the fear that is being priced in by credit markets as an important indicator for equities.

When credit markets signal calm, even while equities are struggling, it is often a sign that equity weakness is more about valuations and positioning and less about growth fears. But if credit market weakness confirms equity market weakness, it can be indicative of deeper growth fears that could come with negative equity events, like cuts to earnings estimates.

We monitor this credit fear by looking at credit spreads (the extra compensation that credit investors demand to lend to riskier borrowers) as well as the pricing of credit default swaps (the price that an investor is willing to pay to insure against default risk). Both of these measures have increased substantially over the last month but remain well below levels seen in recent times of stress, as shown in the two charts below.

As of: 3/14/25

As of: 3/14/25

It must be noted that these credit measures are coincident indicators, so the fact that they are lower than prior peaks today does not give the all-clear for equities. Instead, the more helpful interpretation is one of divergence: if credit spreads are widening as equities are rallying, it is a potentially negative sign for equities, while if credit spreads are narrowing as equities are selling off, it is a potentially positive sign for equities.

To wrap, this look at credit brings up a discussion about earnings estimates. We have been flagging the divergence between equity prices rallying over the last six months and S&P 500 earnings estimates getting cut as creating a “fragile” set up for equities to begin 2025 (we’ve been calling it a “rally on air”, fueled only by PE multiple expansion).

S&P 500 Price and 2025 EPS Estimate

Source: Bloomberg, NewEdge Wealth, as of 3-14-25

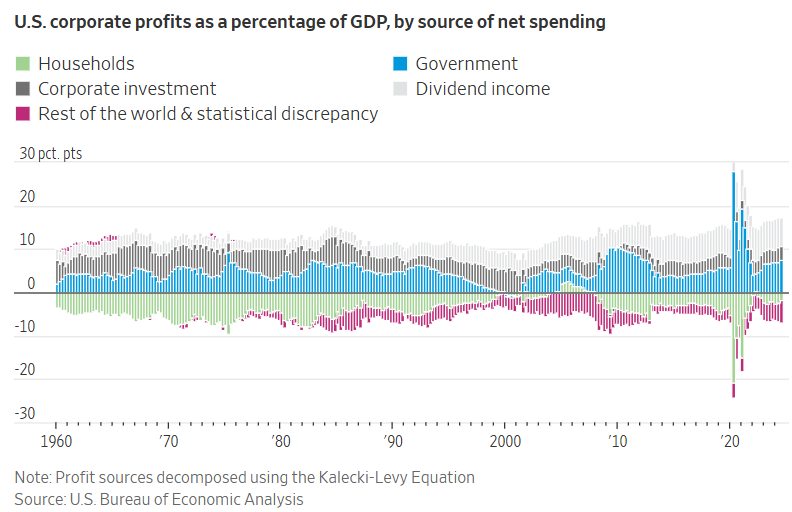

But adding to the earnings estimate revisions we have already seen, the ultimate question is whether the “DC Detox” will result in even weaker corporate earnings than current estimates.

This WSJ article offers a fascinating take, observing that “almost 60% of the corporate earnings generated between 2022 and the third quarter of 2024 can be attributed to public-sector spending and investment”, which suggests that a pursuit of lower deficits, though considered laudable by most in the long run, could result in weaker corporate profits in the short run.

Source: WSJ, 3/12/25

Consensus now expects EPS growth of 10% in 2025 and 12.5% in 2026, so this potential slowdown in corporate profits is currently not being contemplated by forecasters.

The conclusion from this set of “aggregate growth fears” measures is that we have seen growth fears increase in recent weeks, but consensus still expects a relatively robust, albeit slower, environment for US economic growth. We will have to monitor incoming data to see if it confirms these brewing growth fears (which will likely lead to even more downside to estimates), or if it challenges these fears with a more optimistic reality.

“Immunity Long Overdue”: Conclusion

Individual fear is an inevitable emotion when markets are lurching lower and headlines are filled with talk of recession, but as the above analysis shows, when aggregate fear spikes and becomes the consensus emotion, it usually behooves investors to find that “long overdue immunity” to their own individual fears and embrace contrarian optimism.

We have yet to see signs that various fear gauges are at extreme levels seen during other major market lows, which suggests to us that even as markets look to stage a rebound in the short-term, they could remain volatile in the medium-term. Again, this does not mean that there are not opportunities in today’s equity markets after the sharp correction of the last month, but we have tempered expectations for a powerful V-shaped recovery to new all-time highs (as was experienced after 2023 and 2024’s volatility).

Regardless of this near-term volatility, we encourage investors to continue to find immunity to their personal fears and find insight and opportunity in aggregate fears.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2025 NewEdge Capital Group, LLC

The post Fear Inoculum appeared first on NewEdge Wealth.