But you know that we’ve changed so much since then

Oh yeah,

We’ve grown

“Do You Remember the First Time?”, Pulp

This week’s 2024 Election delivered a decisive win for President-Elect Trump and the Republicans, with the party winning a majority in the Senate (there are still House of Representatives races that have not been called, but betting markets, like Polymarket, have a 97% chance of a full Republican sweep).

Risk assets soared higher in response, with the S&P 500 delivering a record post-election rally on Wednesday and its strongest weekly performance of the year (our Brian Nick and Jay Peters put out a great piece earlier in the week post-election).

The price action across equities, fixed income, and currency markets had many investors “remembering the first time” that Trump was elected in 2016, with the assumption that a similar playbook can be applied to today’s market.

However, 2016’s economic and market backdrop is notably different than today’s, while the timing of Trump’s policy priorities is likely to differ as well. To support this point of difference:

• The S&P traded at 16.5x earnings pre-2016 election vs. 22.7x today

• The 10 Year Treasury traded at 1.8% pre-2016 election vs. 4.3% today

• The Fed Funds Rate was 0.5% pre-2016 election vs. 4.75% today

• The Core PCE Inflation was at 1.5% pre-2016 election vs. 2.7% today

• The Unemployment Rate was above 4.8% pre-2016 election vs. 4.1% today

So just as Jarvis of Pulp (who still, by the way, positively brings the house down) croons, “but you know that we’ve changed so much since then,” we raise the question if we should apply the same post-election playbook in the coming months, or if market leadership under a second term for Trump could have a different character (or a Different Class, if we are sticking on the Pulp theme).

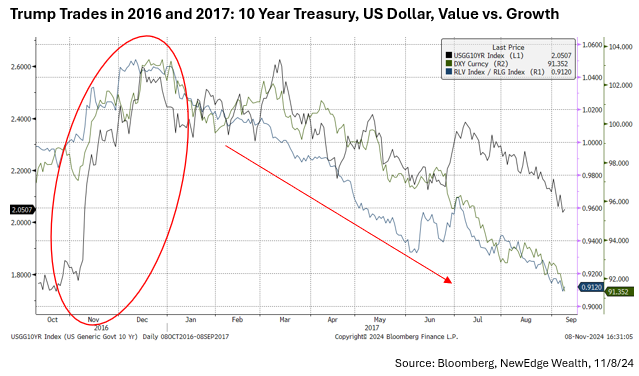

“It’s Half Past Eight, You’ll Be Late”: The Short-Lived Trades of 2016

The starting point of analyzing the 2016 playbook is to appreciate how short-lived these trades were eight years ago.

The initial reaction to Trump’s surprise victory in 2016 was to see stocks surge overall, led by Value equities, while Growth lagged by nearly 5%. Small caps rose a whopping 20%, and emerging markets sold off nearly 10%. The US 10 Year Treasury rose nearly 80 bps, and the US Dollar rose almost 7%.

All of this happened in the two months post-election, but as soon as January 1, 2017, rolled around, these trades began to reverse. Growth began to lead value, small caps began to lag large caps, emerging markets began to outperform, the 10 Year Treasury reversed lower, and the US Dollar began a descent.

The reversal in these trades captures how the initial reaction to Trump’s victory in 2016 was an anticipation of the policies to come, not necessarily the clarity or enactment of the policies themselves. This is a great reminder that oftentimes, the knee-jerk reaction to an event is not the one that persists.

What is not shown in this chart is that some of Trump trades reasserted themselves in late 2016/early 2017 as policies came clearer into vision and were enacted. The 10 Year Treasury began to climb in September of 2017 as deficit-increasing tax cuts were getting closer to passage, while the US Dollar began to strengthen as tariffs were enacted in January of 2018.

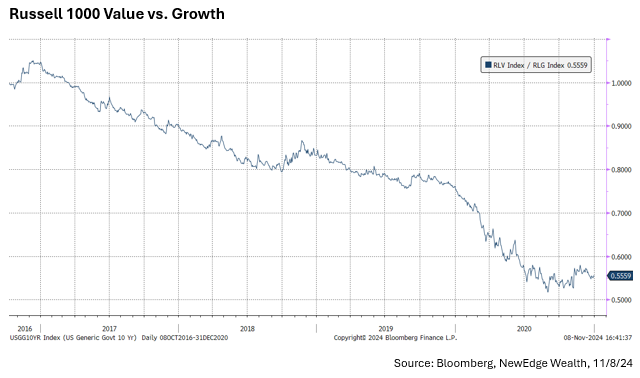

Importantly, cyclical and Value parts of the market never regained their relative footing vs. Growth during Trump’s first term. Value underperformed Growth relentlessly from 2017-2020, as seen in the chart below.

Of course, there are many other factors to Value’s underperformance vs. Growth other than just policies coming out of DC, but this is another great reminder that the initial reaction is oftentimes not the trend that sticks.

“You Say You’ve Never Been Sure”: Today’s Post-Election Trades

We should start by making a couple of broad observations about the market this week (we will put charts to these observations in our Monday illustrated missive):

• The rationale for the jump higher in stock and credit valuations is partially the removal of a “tail risk” to profits from higher corporate taxes and greater regulation that could have come with Democrat control. Lower corporate taxes and/or deregulation that meaningfully impacts profits are not a guarantee but do have a higher probability of happening under Republican control.

• The S&P 500 and other major large cap indices remain in powerful uptrends, with a surge in breadth for the broad market this week, as measured by the Russell 3000’s 20-day highs hitting 55%, a measure that is often followed by strong forward returns.

• The S&P 500 is technically overbought, so some digestion could come in the near-term, but these breadth and strong uptrend characteristics are not consistent with an ultimate “top” in equities.

• There is, however, a troubling divergence brewing within equities that should be monitored: equities are pressing higher on valuation expansion alone (the S&P is trading at 22.6x forward, nearly to the 2020 peak!), with forward earnings estimates for 2025 getting trimmed (EPS for 2025 now at $272 vs. $277 in August).

• Credit spreads have reached new cycle lows, with the High Yield spread at just 305 bps, it is now below its tightest level even going back to 2021. Credit is priced for ultimate perfection.

• All in all, financial conditions have eased as yields and the dollar reversed some of their gains, and equities and credit have seen valuations rise.

The initial reaction to the Republican victory was a repeat of the 2016 trade: Cyclicals outperformed Defensives, Small Caps outperformed Large Caps, yields moved higher, and the US dollar strengthened. Some of these moves lasted only one day, though, with reversals on Thursday and Friday in areas like the 10 Year Treasury yield, which finished the week only slightly higher than it started.

We think the key to evaluating the durability of these Trump trades is to judge the likelihood that the power balance and policies coming out of DC over the next four years will have an impact on the trajectory of fundamentals. Said another way from an equity perspective, if it is not going to impact earnings, it is not going to last.

This is where we will have to judge the potential policy offsets of what is welcomed by stocks (the potential for lower taxes and deregulation) and is a challenge to stocks (tariffs and immigration).

The order of this matters as well: in 2017, stocks were strong in anticipation of a big cut to corporate taxes but then traded weak in 2018 as tariffs were enacted (and the Fed drained liquidity). This time around, tariffs could and may be enacted early in Trump’s second term, while lowering corporate taxes may be a greater challenge as we near 2026, given the $4T of taxes that are already set to be negotiated later next year.

We will also have to judge if the backdrop of potentially stronger growth and inflation that comes with higher/stickier yields is supportive of these trades.

For example, small caps have been rallying on a pro-growth, pro-cyclical narrative, with lower taxes and increased M&A from deregulation as possible tailwinds.

We see small caps as needing a combination of both resilient growth and lower yields in order to have sustained outperformance. Small cap stocks have higher usage of floating rate debt and higher overall debt levels, making the recent environment of elevated rates a challenge for the group’s profitability (the Russell 2000’s estimated EPS growth for 2024 has been cut from +10% to start the year to -22% today). If we look at consensus estimates for 2025, the Street has an expected 40% growth rate baked in for next year. 2024’s weak performance is certainly an easy “comp” from a year-over-year perspective, also called a low bar to jump over, but in order to achieve that 40%, companies likely need to see continued strong economic growth and relief on their cost of debt with falling interest rates. It certainly is a “show me” story, meaning the recent rally in small caps based on valuations and a positioning chase should constantly be checked to make sure that there is building evidence for a rebound in earnings.

There are many other areas of the market to dissect in this manner, which is an exercise we will do over the coming weeks in this Weekly Edge. Suffice it to say that narratives may move prices in the short term, but we will continue to examine where policy proposals and the concomitant sentiment/behavior shifts can move fundamentals in the long term.

Bonus Thoughts on the Fed from Brian Nick:

The other policy news this week came from the Federal Reserve, whose headquarters is located just a few blocks from the White House. The Fed delivered on expectations, cutting its policy rate by 25bps to a 4.5% to 4.75% range. The accompanying statement noted that risks to inflation and employment are roughly balanced, though labor market conditions have “eased” and inflation remains somewhat above the Fed’s 2% target. In his presser, Powell was evasive on the near term path of rates but appeared committed to getting rates down to “neutral” in this cycle, contingent on the data.

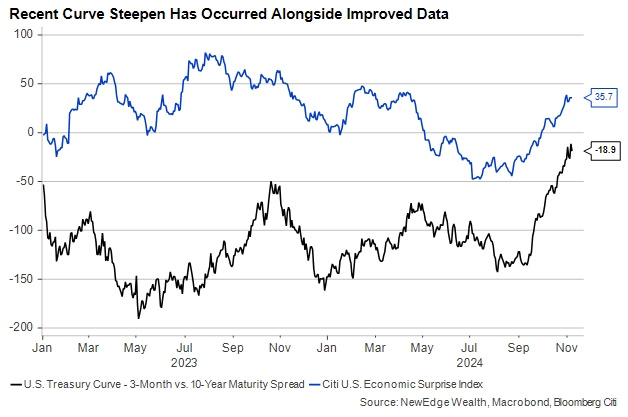

Given its placement in the choppy wake of the U.S. election and the certainty of the outcome, yesterday’s FOMC meeting was not as keenly anticipated as others. The economic data since the Fed’s September meeting has shown strength in consumers and weakness in other areas, like housing. On the whole, upside economic data surprises have contributed to rising longer-term rates and the steepening U.S. Treasury yield curve.

It’s been puzzling to see long-term rates rise with short-term rates finally beginning to move down. Rising long-term yields could signal that today’s rate cuts are seen as contributing to higher rates in the future as a result of stronger growth or hotter inflation (or both). The election has played a part, as well, but whatever the cause, the rise in long-term rates since September has been unwelcome news for large swaths of the economy.

Has the Fed’s move to lower rates been self-defeating? Mortgage applications for purchase are back down close to twenty-year lows, with 30-year borrowing rates well above 7% again. Real industrial output has been flat for over two years. And last week’s GDP release showed commercial construction falling for the first time since 2021.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2024 NewEdge Capital Group, LLC