Introduction

“It burned like fire, this burnin’ desire”

The U.S. economy grew at a solid 2% rate in the first quarter, and equity market indexes are making new all-time highs. Yet consumer and small business outlooks remain subdued. This divergence is nothing new, but the unique nature of the April market rally (which we’ve been writing about over the past few weeks) may help to explain why markets still feel fragile and brittle despite good economic and financial market headlines.

Having come into 2026 expecting a strong and broad cyclical upturn, investors still haven’t found the economy they’ve been looking for. Consumer resurgence – led by the promise of stimulus and lower interest rates – has been downgraded to consumer resilience. And the expected booms in construction and manufacturing, carrying with them the promise of broadening growth and market participation, have not materialized. Instead, we remain in a “good enough” economy propped up by incredible growth in technology investment and an unsustainable drop in the household savings rate.

“I Still Haven’t Found What I’m Looking For” is the second U2 song (and the second from 1987’s The Joshua Tree) we’ve used as inspiration for a Weekly Edge. Ironically, the first one came in early 2025 as the so-called A.I. trade was looking wobbly and we questioned whether the stock market could carry on without it. Our concerns turned out to be unfounded, but we’re back today asking a different question: can the A.I. trade keep the economy and the markets going as other sectors falter.

The Economy We Were Promised

“I have climbed the highest mountain”

We entered 2026 optimistic about U.S. economic prospects. Most of the tax cut provisions from the One Big Beautiful Bill Act (OBBBA) had yet to kick in. The hit from tariffs was smaller than expected and was receding into the rearview mirror. Interest rates had come down in the second half of 2025 and continued to do so during the first two months of 2026. This had the potential to unlock the frozen housing market and make construction projects of all types more attractive to take on.

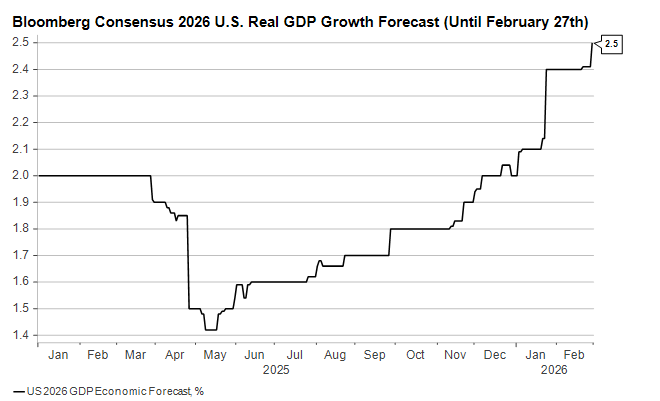

This graph of the Bloomberg 2026 U.S. GDP consensus as of February 27th shows how dramatic the upward revisions to the outlook had been:

Amid the improving forecasts, we were wary of two risks. The first was that the labor market was teetering with monthly hiring approaching zero. The second was that equities were priced for perfection based on earnings expectations that might be hard to achieve.

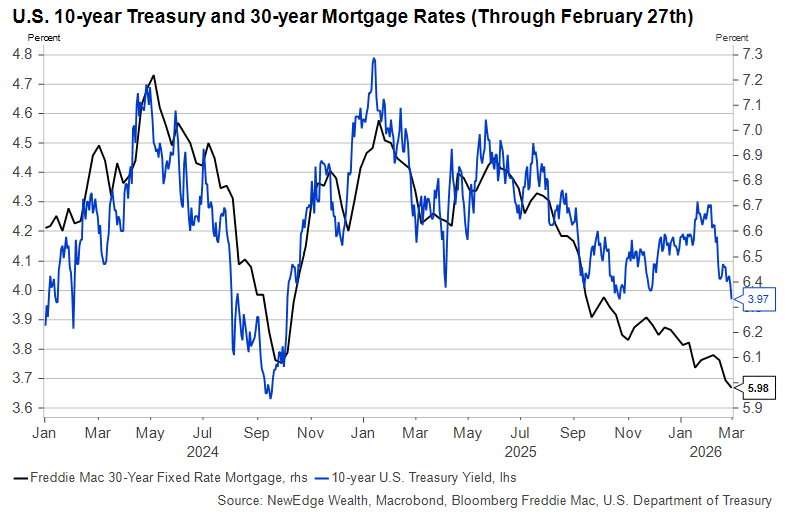

These risks were partly assuaged by our view that the policy environment would continue to become more accommodative, stirring broader hiring and stronger personal consumption. Falling interest rates, which also helped bring 30-year fixed rate mortgage rates below 6% by the end of February, were particularly encouraging:

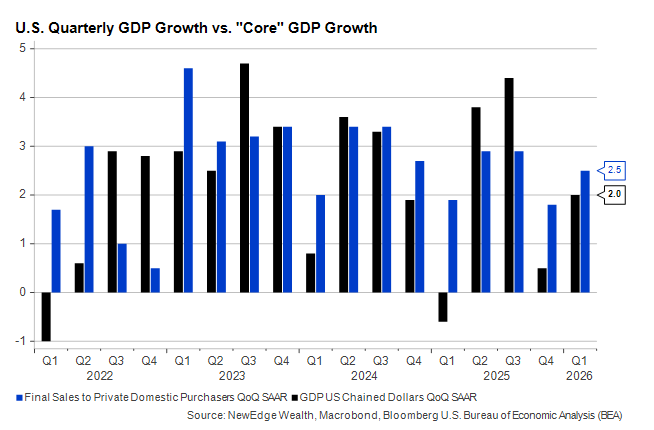

This past week’s release of the Q1 GDP confirmed that the U.S. economy entered the year with some positive momentum. Growth accelerated compared to Q4 of last year:

Some of this had to do with the timing of the government shutdown, which detracted from Q4 GDP and then added to it as federal workers returned. But final sales to domestic private purchasers (i.e., not the government), also show improvement. Even so, as we will lay out in the next section, these hopeful numbers do not show the bulk of the likely eventual impact from the Iran War, and they mask how narrow economic growth has become.

We’re Not Going Back to February 27th

“I have run, I have crawled”

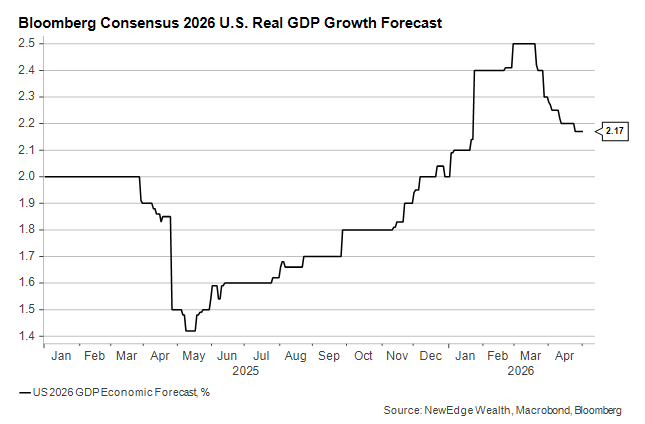

The onset of the Iran War has driven two crucial economic inputs, oil prices and interest rates, significantly higher. While not fatal, gasoline above $4.25 per gallon and a 10-year U.S. Treasury yield once again approaching 4.5% are spoiling what was supposed to be a year of stronger and broader growth. Indeed, when we update the Bloomberg consensus chart from earlier to show the last two months, we can see what may just be the beginning of the fallout:

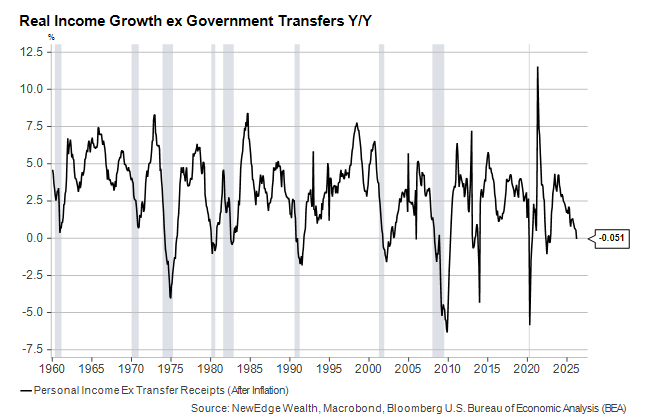

The economic impact so far from the Iran War is stretching U.S. consumers. Real incomes excluding government transfers were already growing at a snail’s pace, but March’s high inflation reading brought them into negative territory over the past year, something that rarely happens outside of recessions:

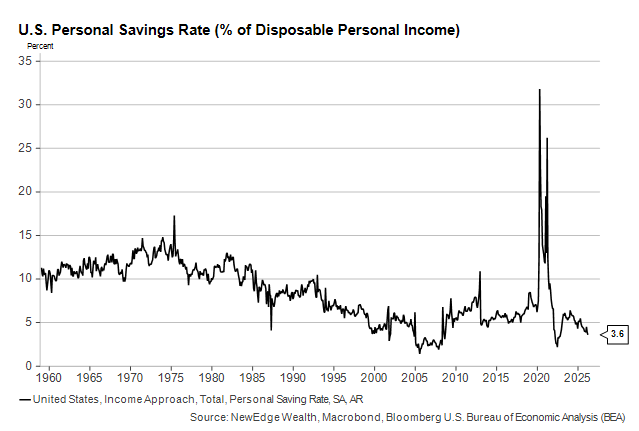

Considering that real incomes fell during Q1, consumer spending held up rather well. In fact, personal spending growth was positive in March even after accounting for unusually high inflation. Of course, this math only works if households save less of what they earn, and that’s precisely what they’re doing. The personal savings rate, at 3.6%, is down a full 1.5% since the start of 2025:

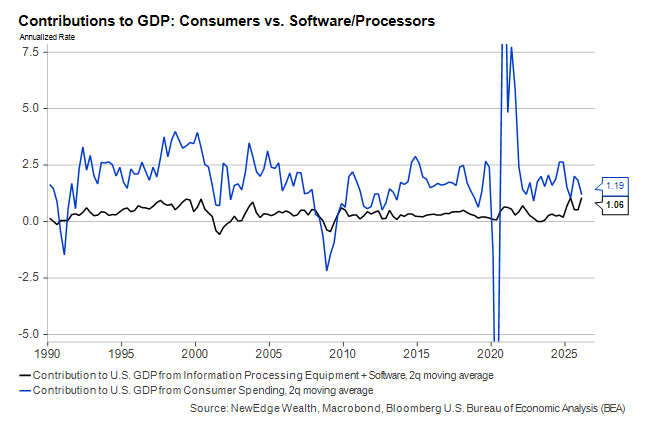

The other standout feature of the Q1 GDP data was how heavily the growth relied on private business investment in a narrow set of categories, including software and information processor equipment (i.e., chips and computers). While these constitute a far smaller percentage of overall U.S. economic output than does consumer spending, A.I.-adjacent investment has accounted for nearly as much of the economic growth as consumption in recent quarters:

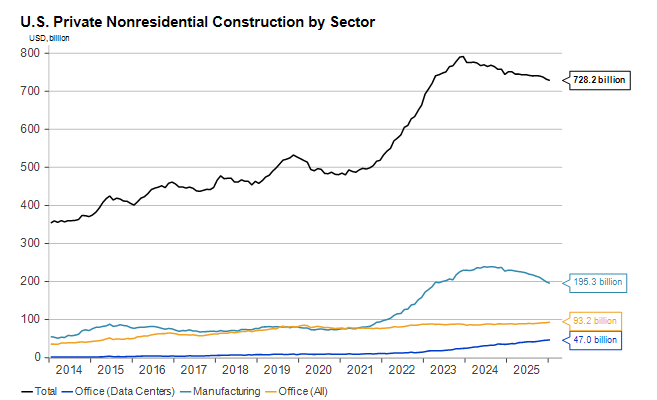

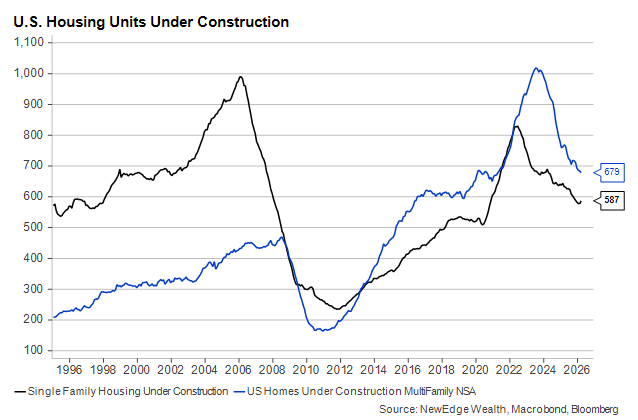

Meanwhile, spending on commercial structures outside of data centers (e.g., factories) continued to drop, as did spending on new single- and multi-family housing, which fell for the fifth straight quarter. Total non-residential construction spending peaked in early 2023 as the 2021 infrastructure bill took effect, and data centers (the blue line on the graph below) have been the only significant source of positive construction growth since then:

March showed a small tick up in single-family homes under construction, but the number of housing units being built has fallen significantly over the past several years:

The story of the U.S. economy at the start of May 2026 is one of exploding growth in a narrow array of sectors, stiff headwinds for U.S. consumers, and near-recessionary conditions in many other areas. That’s different than what most economists expected coming into the year.

Better Labor Market Removes a Tail Risk

“But yes, I’m still runnin’”

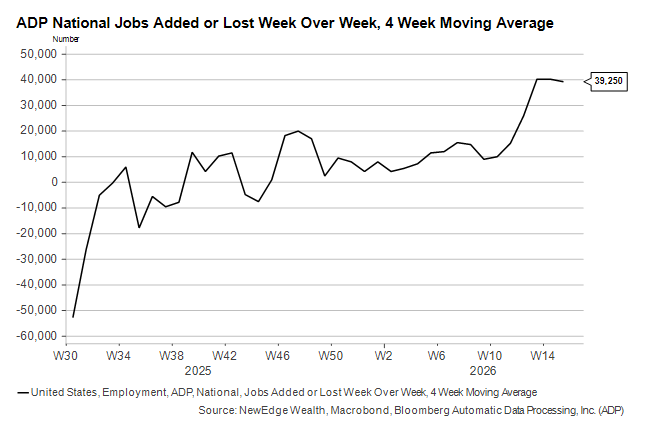

If there has been a bright spot in the U.S. economy relative to original year ahead expectations, it has been in the labor market. Weekly payroll growth has improved, according to ADP:

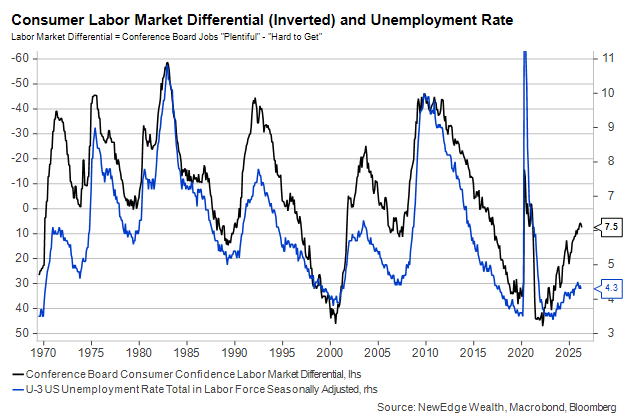

To corroborate this, weekly jobless claims have fallen to their lowest since March of 1969. And consumers no longer report feeling worse about the jobs market than they did a month ago, a promising break in what had been a worrying trend in this series:

Together, this data indicates that the BLS’ upcoming report on the job situation in April will be solid. We had feared that unemployment might be high enough by now to tempt the Fed to cut rates, but we learned last week that they’re further from doing so than they have been in some time.

Conclusion: Narrower Growth, Narrower Markets

“Then all the colors will bleed into one”

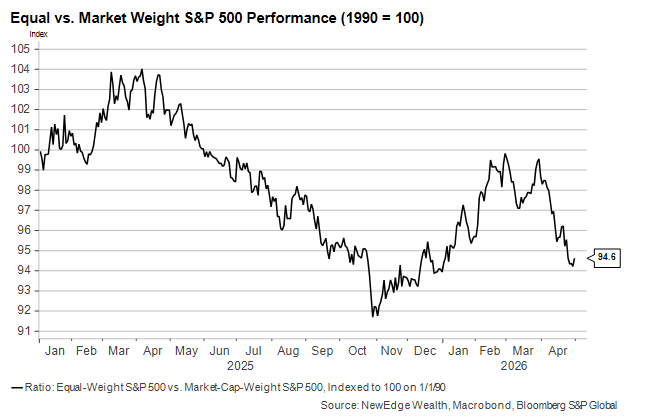

The other bit of promising news this year has been that earnings estimates have outpaced stock prices, causing valuations on indexes like the S&P 500 to remain steady, on net, despite positive market gains. As we have pointed out in prior Weekly Edges, however, much of the improvement in earnings forecasts has been in a small number of companies that produce (you guessed it) hardware connected to the growth in A.I. investment and usage.

In this way, the markets and the economy are in harmony. Narrower growth is creating narrower market leadership, leading the already-very-large technology firms to see outsized returns. This explains the large recent drop in the series we show on the next graph, which rises when the market is broadening (i.e., when the very largest stocks are not outperforming the average stock) and falls when it is narrowing:

Earnings season is still underway, but firms in the A.I. space are unanimously delivering earnings reports that beat lofty expectations, leading analysts to continue raising their forecasts. We cannot always foresee market turns before they happen, but there is not much in the economy at the moment to make us think that a) economic growth is about to accelerate or broaden; or b) that the so-called “A.I. trade” is running out of steam given rising capital expenditures and computing power demand still outpacing supply.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC

The post We Still Haven’t Found What We’re Looking For appeared first on NewEdge Wealth.