Heat lighting flash, but don’t blink

Misleading

Tranquility ruse

You’re gonna happen again

That’s what I think

Follow the evidence

Look it dead in the eye

You are darkness

Trying to lull us in, before the havoc begins

Into a dubious state of serenity

“7empest”, TOOL

Just as markets were trading “calm as cookies and cream” as they celebrated benign inflation prints, better-than-expected earnings, and resilient economic data, geopolitical events on Friday ushered in a “tempest”, rattling global markets out of their “dubious state of serenity”.

The conflict between Iran and Israel caused a spike in oil, a drop in stock prices, and a rally in safe haven assets like gold and the USD. Notably, U.S. Treasuries, a prototypical safe haven asset, did not rally on Friday, with yields across the Treasury curve (2 year, 10 year, 30 year) all pressing higher on the day.

To avoid becoming “victims of our own certainty”, we are going to unpack each of these market moves in the sections below.

“So Try as You May, Feeble Your Attempt”: Oil Price Reaction

The below analysis about markets hinges on the path forward for oil prices. Oil, which rallied ~8% on Friday, is the key determinant if this geopolitical event is something markets will “look through”, as they most often do, or if there will be a longer-lasting impact.

We start with the most objective read on oil by using technical analysis. The chart below shows how oil has been in a distinct downtrend since mid-2022 and is now very overbought (using the relative strength index in the bottom panel).

WTI Oil Price per Barrell

The combination of being overbought into downtrend resistance suggests that oil doesn’t deserve the benefit of the doubt to press higher from here, but we have to be on watch for signs of a brewing trend change (these would include new multi-year highs, higher lows, and strong reactions at support levels).

Watching for a trend change in oil prices is so very important because the downtrend in oil prices has been hugely beneficial to U.S. disinflation and consumer spending over the last few years.

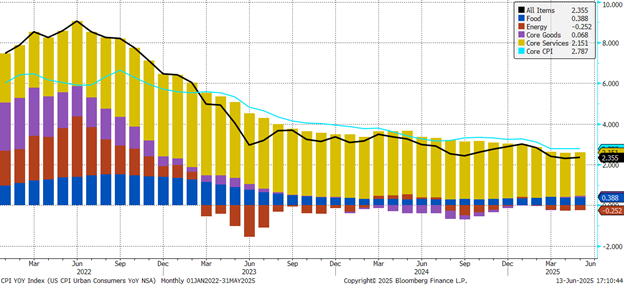

First on the inflation front, the red bars in the chart below show how energy has gone from being a huge contributor to CPI inflation back in 2022 (when CPI hit a peak of 9.1% in June of 2022) to being a key detractor from inflation over the past two and a half years. A meaningful change in the trajectory of oil prices might cause Headline CPI readings to inflect higher, a development that would not be welcome by the Fed.

CPI Components: Bloomberg ECAN

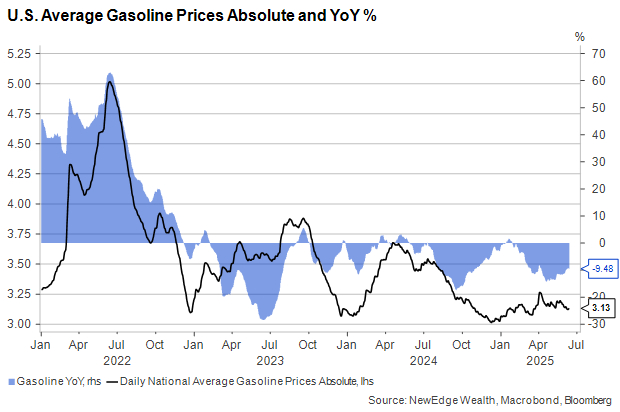

On the consumer front, we think of energy/gasoline prices as effectively a tax on consumers. Energy consumption is inelastic (meaning people keep buying even as prices go up) and largely non-discretionary, so when energy costs spike, consumers tend to cut spending in other areas.

However, over the past two years, gasoline prices have been generally falling, with negative YoY changes in gasoline the norm since early 2023 (chart below). This has provided a boost to consumers, freeing up money for spending in other areas. But if gasoline prices were to sustainably climb higher, we would expect household consumption in other areas to get pinched.

Of course, there is a big “if” in the sentence above, meaning that it is not a given that this geopolitical event will cause a sustained rise in oil prices.

The consensus from oil and geopolitical experts is that there is ample latent oil production capacity that can be brought online in response to higher prices. Further, analysts have pointed out that no Iranian production capacity has been targeted at this time. But if this fighting continues, analysts will be watching closely for conflicts in the Strait of Hormuz and Kharg Island (where Iran processes 90% of its crude oil exports).

History shows that a sustained rise in oil prices is the key differentiator between a geopolitical event that markets “look through” and a geopolitical event that has lasting impacts. Examples, such as the 1973 OPEC Oil Embargo in response to the Yom Kippur War (oil prices more than tripled) and more recently the 2022 Russian invasion of Ukraine (oil prices rose 35% to their June 2022 peak) are stark reminders that higher oil can act as an exogenous shock on an economy and cause significant headaches for policymakers.

It is far too soon to make a call if this is a trend change for oil, but we will stay disciplined with the technicals above to look for signs that the beneficial downtrend in oil is starting to turn.

“Tranquility Ruse”: Stock Price Drop

To emphasize again, the main factor on whether or not this geopolitical event will impact equity markets will be the price of oil. If oil prices fade quickly, equity markets will move on to the next topic du jour (Tariffs! OBBB! AI! Earnings!).

However, it is important to note that equities may have fallen for a “tranquility ruse” recently, having experienced the largest ever plunge in volatility as measured by the VIX index on record over the last six weeks.

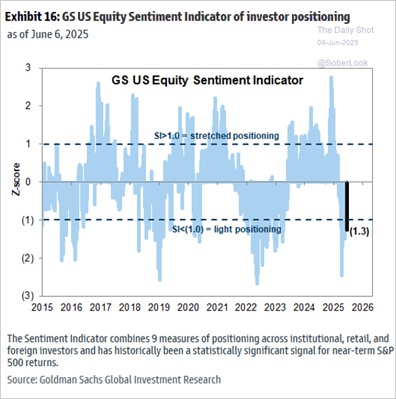

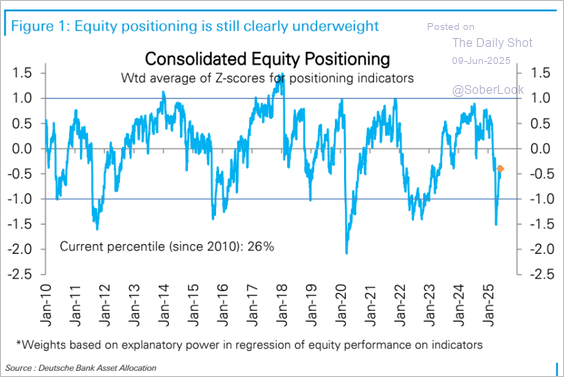

We have been flagging continuously light institutional equity positioning from both the Goldman Sachs and Deutsche Bank measures (both shown below as of the end of last week), which suggested that the pain trade was still higher for stocks.

However, as stocks rallied sharply off lows and reached near-prior-peak valuations of 22x forward earnings, we have argued that the “easy part” of the rally is likely done and that volatility could return as we enter what we have been calling “The Summer of Mud” (a period of muddy economic data, murky policy, and clouded conviction in equities).

We return to technicals to keep it objective, looking to 5700-5800 as the first level of important support for the S&P 500 to hold. Due to the light institutional positioning, dips may be readily bought, but again, it depends on the magnitude and duration of the oil price reaction to these geopolitical events.

“We Know Your Nature”: Safe Haven Rally

Thank goodness the USD rallied Friday. The lack of a USD rally on a “risk-off” geopolitical event day would have caused us to raise our eyebrows even further about the meaning behind recent pronounced USD weakness (just on Thursday, the DXY broke below 98 to a new YTD low).

The inability of the USD to rally alongside US stocks over the past two months has been a curious development that suggests that some of the concerns about waning demand for US-based assets (either for international trading or foreign reserves purposes) may have some truth to it at the margin.

We have been flagging that positioning has been a key driver of USD weakness, with USD positioning flipping from max-long at the start of the year to max-short today. Due to the short positioning, it is not surprising to see a USD rally as traders get caught in a short squeeze.

International Money Market USD Positioning and DXY

“And Therefore, Your Doubt’s Not an Option”: Treasury Market Sell-Off

Just as an enigmatic lyric from TOOL sparks debate amongst fans (TOOL is famously known for not clarifying the meaning behind lyrics and titles in order to keep the lanes of interpretation open for fans), the move in Treasuries has sparked debate amongst market watchers as to how a rise in yields in the face of a “risk-off” event should be interpreted.

Our view is that the rise in the front end (2-Year yield) reflects the potential that higher oil prices, and thus a potential reacceleration in headline inflation, could hamper the Fed’s ability to deliver the market’s hoped-for rate cuts through the end of the year.

Our view on the rise in the long end (10 Year yield) reflects this risk of persistently stickier inflation that makes ballooning budget deficits even less palatable to long bond investors (recall our “Era of Consequence”) and reduces their perceived safety in a risk-off environment that has an inflationary component to it (read: stagflation). We think that this 10-Year yield move shows that the bond market, at least on Friday, is more concerned about inflation than it is about growth.

As we wrote recently, we still believe that bonds will provide diversification benefits in the next economic downturn, but that the data has to get much worse before it gets better in order to spark a sustained flight to safety in these assets due to lingering inflation and high deficit spending.

“A Tempest Must Be Just That”: Conclusion

As Maynard screams at the beginning of “7empest”: “Here we go again!”

The calm that markets enjoyed coming out of the April lows seems to be hitting a wall, for now, but as we have frequently written this year, volatility provides opportunities to investors for rebalancing and deploying portfolios.

It is highly uncertain (or muddy) what duration or magnitude recent geopolitical events will carry for markets, with oil prices being the key watch item for how markets will digest these developments.

We will continue to objectively assess these developments, aiming, as always, to avoid “becoming victims of our own certainty”.

IMPORTANT DISCLOSURES

All data is as of June 13, 2025, unless otherwise noted.

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2025 NewEdge Capital Group, LLC

The post 7empest appeared first on NewEdge Wealth.